If you have ever thought about investing in stocks, mutual funds, or bonds in India, a demat account is where that journey begins. This guide covers everything you need to know about what a demat account is, how it works, what it costs, and how to get started

What is the meaning of Demat Account?

A demat account (or a dematerialized account) is an account where your shares and securities are held electronically. But beyond just storing your investments, the use of a demat account extends to buying, selling, and transferring securities digitally and safely, all from one place.

They can also hold a wide range of financial instruments such as bonds, government securities, mutual fund units, ETFs (exchange-traded funds) and more.

SEBI has made a demat account mandatory for holding and trading most securities in electronic format in the Indian stock market.

Also Read - Demat Account Full Form

History of Demat Accounts in India

To understand the purpose of demat account, it helps to know why it was created in the first place.

Before 1996, investing in stocks meant holding physical share certificates as proof of ownership. This came with serious drawbacks. Certificates could be stolen, destroyed, or forged, and transferring ownership involved significant paperwork and delays.

The Depository Act of 1996 provided the legal framework for the concept of holding shares in electronic format.

Following this, India’s first electronic depository, the National Securities Depository Limited (NSDL) was established in November 1996. NSDL made it possible to hold share securities in digital format for the first time in India.

In 1999, a second depository, promoted primarily by BSE (Bombay Stock Exchange), came into the picture. It was the Central Depository Services Limited (CDSL).

Today, every demat account is held with either NSDL or CDSL.

Features and Benefits of a Demat Account

As an investor, these are the features and benefits of a demat account that you should know about:

- Faster settlements: When you buy stocks today, it is credited to your account following the next business day under India’s T+1 settlement system for most investments like equity shares, ETFs, bonds, REITs, and InvITs.

- Every asset, in one place: Every kind of asset that you own, be it stocks, bonds, ETFs, government securities, mutual fund units, or sovereign gold bonds, is all consolidated under your demat account. You get to view, access or trade your securities all under one account.

- Corporate benefits are credited automatically: When a company declares a dividend, stock splits, issues bonuses and makes a rights offer, the relevant credits or information are automatically updated into your account. No need to track it manually.

- Loan against securities: If you have a substantial portfolio and you need short-term liquidity, you may pledge your securities and keep them as collateral, without selling them. The terms, interest rates, loan limits and eligibility criteria vary across lenders and depend on the securities pledged.

- Multiple layers of security: While your securities are already secured under the depository system, your account access is protected through multiple layers of security such as Two-factor authentication, OTP-based login, biometric verification on mobile apps, and transaction alerts via SMS or email.

- Accessible anywhere: Most depository participants have mobile apps that give you access to your demat account, allowing you to view your portfolio, place orders, and manage your account from anywhere.

- Freezing your account: If you suspect unauthorized activity or simply want to ensure no transactions occur on your account for a period of time, you can request a freeze through your DP. A freeze restricts debits, credits, or both, depending on the type you apply, without affecting the value of your holdings in any way.

Also Read - What is Trading Account

Demat Account Opening Documents

Here are the documents you require to open a demat account:

1. Identity Proof:

- PAN Card (Mandatory for all kinds of securities transfer in India)

- Aadhar card

- Passport

- Voter ID

2. Address Proof:

- Aadhar card

- Utility Bills (Electricity, water or gas bill not older than 3 months)

- Bank passbook or bank account statement

- Ration Card

3. Bank Account Details:

- A cancelled cheque (with your name printed on it)

- Recent bank statement or bank passbook copy (bank account linked with demat account)

4. Passport-sized photograph

5. Income Proof (for F&O trading)

- Recent ITR acknowledgement

- Six months' bank statements

- Pay slips

- Form 16

Read - Documents required for demat account

How Does a Demat Account Work?

Here is what happens from the moment you make a trade till the moment the securities are credited to your account:

- Step 1: You place an order through your trading account to sell or buy a security.

- Step 2: The order goes through the stock exchange, either NSE or BSE, where it matches with a seller or buyer at the agreed price.

- Step 3: India currently follows the T+1 settlement for most of the trades, which means the settlement of the trade takes place one business day after the trade date.

- Step 4: Once the settlement cycle completes, the shares are credited to your demat account by your DP.

If you sell, the shares are debited from your demat account and credited to the buyer’s account after one business day. Also, the sale proceeds are credited to your account after one business da

Types of Demat Accounts in India

These are the primary types of Demat accounts in India:

- Regular Demat Account: This is the standard demat account for Indian residents. You can hold stocks, bonds, ETFs, mutual funds, government securities, and more in electronic form, with no restrictions on the type of securities you hold or the volume of transactions you make.

- Repatriable Demat Account: This comes under NRI demat account, which is designed for Non-Resident Indians (NRI). This allows them to invest in Indian markets and move their funds, both the invested amount and returns, back to their country of residence. It must be linked to an NRE (Non-Resident External) bank account.

- Non-Repatriable Demat Account: This demat account also comes under NRI demat account, but unlike the repatriable type, funds invested through this account cannot be moved outside India. It is linked to an NRO (Non-Resident Ordinary) bank account, and any proceeds from securities sold can only be reinvested within India.

- Basic Service Demat Account (BSDA): A cost-effective alternative to the regular demat account, designed for investors who trade or invest infrequently. Since SEBI periodically revises BSDA eligibility criteria and fee structures, check the latest guidelines with your DP. Note that you cannot hold more than one BSDA account against your PAN.

Beyond individual accounts, demat accounts can also be held by or on behalf of specific entities, such as a minor demat account, a corporate demat account, an HUF demat account, an LLP demat account and a partnership demat account.

Demat Account Number and DP ID

When you have successfully opened your demat account, you are assigned a unique 16-character account number. Understanding the demat account format helps because this number is used in every securities transaction and is how the depository system identifies you.

The format of your demat account number depends on which depository your broker is registered with, CDSL or NSDL. Here is how the two differ:

CDSL vs NSDL Account Format

| Format | CDSL | NSDL |

|---|---|---|

| Account Number Format | 16-digit numeric number | "IN" prefix + 14 digits |

| Example | 1234567887956423 | IN47368696536797 |

| DP ID | First 8 digits (12345678) | "IN" + next 6 digits (IN123456) |

| Client ID | Last 8 digits (87956423) | Last 8 digits (96536797) |

Note: Your DP ID identifies the Depository Participant, the broker or bank through whom your demat account is held. Your Client ID is the part that is identifying you as an individual account holder. Together, they form your complete demat account number.

Also Read - What are DP Charges

Demat Account Charges

Opening a demat account is generally free, though some brokers may charge a nominal one-time fee. But there are certain maintenance charges and transaction fees that you need to be aware of.

Opening a Demat account is often free or even if it's charged, it usually requires a nominal fee. Other than the opening fees, there are various fees associated with maintaining and using it. Some common Demat account charges include:

- Annual Maintenance Charges (AMC)

- Transaction Charges

- Debit Transaction Charges

- Dematerialization Charges

- Rematerialization Charges

- Pledge Charges

- POA (Power of Attorney) Charges (Many brokers now use alternative authorization methods such as TPIN-based verification.)

- Custodian Fees

- Failed Transaction Charges

- Account Closure Charges

- Stamp Duty

Demat Account 2FA (Two Factor Authentication)

You may have come across the term two-factor authentication for a demat account and wondered what it actually involves. It simply means that to log in to your demat or trading account, you need to verify your identity in two separate forms rather than just entering the password. SEBI has mandated two-factor authentication for all trading or demat accounts in India. Every broker and DP is required to implement it without exception.

When it comes to a demat account, the two factors work like this:

First factor - Something you know: This is your password and your PIN. Something that only you are supposed to know.

Second factor- Something you have: The second authentication factor may include an OTP sent to the registered mobile number or email, a device-based authentication method, biometric verification, or other SEBI-compliant mechanisms.

Demat Glossary

New investors tend to encounter a cluster of terms or finance glossary when first exploring demat accounts. Here is a quick reference for the ones that come up most often:

Dematerialization: The process of converting physical share certificates into electronic form and crediting them to a demat account.

Rematerialization: The reverse process; converting electronically held securities back into physical certificates.

Depository: The institution that maintains electronic records of all securities in India. There are two: NSDL (National Securities Depository Limited) and CDSL (Central Depository Services Limited).

Depository Participant (DP): A SEBI-registered intermediary that can be a broker, bank, or financial institution through whom investors open and operate demat accounts. Acts as the link between the investor and the depository.

DP ID: The unique identifier assigned to a Depository Participant. Forms the first part of your demat account number.

Client ID: The unique identifier assigned to you as an individual account holder. Forms the second part of your demat account number.

KRA: KRA full form in demat account is KYC Registration Agency. When you open a demat account, you need to go through a process called KYC, which verifies your identity. KRAs are SEBI-authorized agencies that store your KYC information centrally.

CML: CML full form in demat account is Client Master List. This is a document issued by your depository participant when your demat account is live. It contains your officially registered details: name, address, PAN, linked bank account and nominee information.

DP: Full form of DP in demat account is Depository Participant. This is the entity through which you open your demat account. It can be a SEBI- registered broker, bank or other financial institution. The DP doesn't hold your securities itself; it acts as an intermediary between you and the central depository (either NSDL or CDSL), which is where your holdings are actually held.

ISIN (International Securities Identification Number): A unique 12-character alphanumeric code assigned to each security. Used by the depository system to identify specific securities in transactions.

T+1 Settlement: India's current settlement cycle. Trades are settled one business day after the trade date and shares credited or debited, and funds transferred, by the end of the following business day.

AMC (Annual Maintenance Charge): The yearly fee charged by your DP for maintaining your demat account.

Conclusion

A demat account is the foundation of your investing journey in India. Whether you are buying your first stock, holding bonds, or building a long-term portfolio, everything goes through your demat account. It is where your investments are held, where your returns are credited and where your financial assets are kept safe.

With Aadhaar-based KYC, zero account opening fees, and mobile-first broking platforms, opening a demat account today takes minutes rather than days.

What matters now is making an informed choice, picking the right broker for your needs, understanding the charges involved, and knowing how the system works before you put your money in. This guide has aimed to give you exactly that foundation.

FAQ

Q - Is two-factor authentication required when opening or using a demat account, and how strict are brokers about it?

Ans - Yes, two-factor authentication is mandatory. SEBI has made 2FA a regulatory requirement for all demat and trading account logins in India, which means every broker and Depository Participant is legally obligated to implement it.

Q - Which factors are driving the growth of demat accounts among Indians, and where can I compare numbers across providers?

Ans - Several factors are driving the growth of demat accounts in India, including increasing financial awareness, easy online account opening, widespread smartphone and internet access, growing participation in IPOs, and the rise of brokers that offer low-cost investing.

Q - What Is the Eligibility to Open a Demat Account?

Ans - Indian residents who are at least 18 years of age, hold a valid PAN card, and can complete the KYC process.

Minors (below 18 years): They can have a demat account, but it must be opened and operated by a parent or court-appointed guardian on their behalf.

Non-Resident Indians (NRIs): Indians not residing in India can open an NRI Demat Account.

Entities such as companies, Hindu Undivided Families (HUFs), Limited Liability Partnerships (LLPs), partnership firms, and trusts are also eligible to hold demat accounts.

Q - Is a Demat Account Safe?

Ans - Yes, a demat account is safe.

Your securities are held by one of India's two central depositories, NSDL or CDSL, which are regulated by SEBI and operate under strict legal and operational frameworks. If your broker shuts down or faces any operational issues, your holdings in your demat account are not affected.

Q - Can I have multiple Demat accounts?

Yes, you can have multiple demat accounts, provided each account is opened under a different broker and linked to your PAN.

Q - What’s the difference between a demat account and a trading account, and which should I open first in India?

A trading account is what you use to place buy and sell orders on the stock exchange. When you decide to purchase shares of a company, you place that order through your trading account.

A demat account is where your securities are stored once a transaction is complete. When your buy order is executed and settlement is done, the shares are credited to your demat account. When you sell, they are debited from it.

As for which to open first, you don't need to choose. Most brokers in India open both accounts simultaneously as part of a single sign-up process.

Disclaimer: This article is for educational and informational purposes only and should not be considered investment, financial, or trading advice. Investments in securities are subject to market risks. Always conduct your own research and consult a qualified financial advisor before making investment decisions.

Related Blog

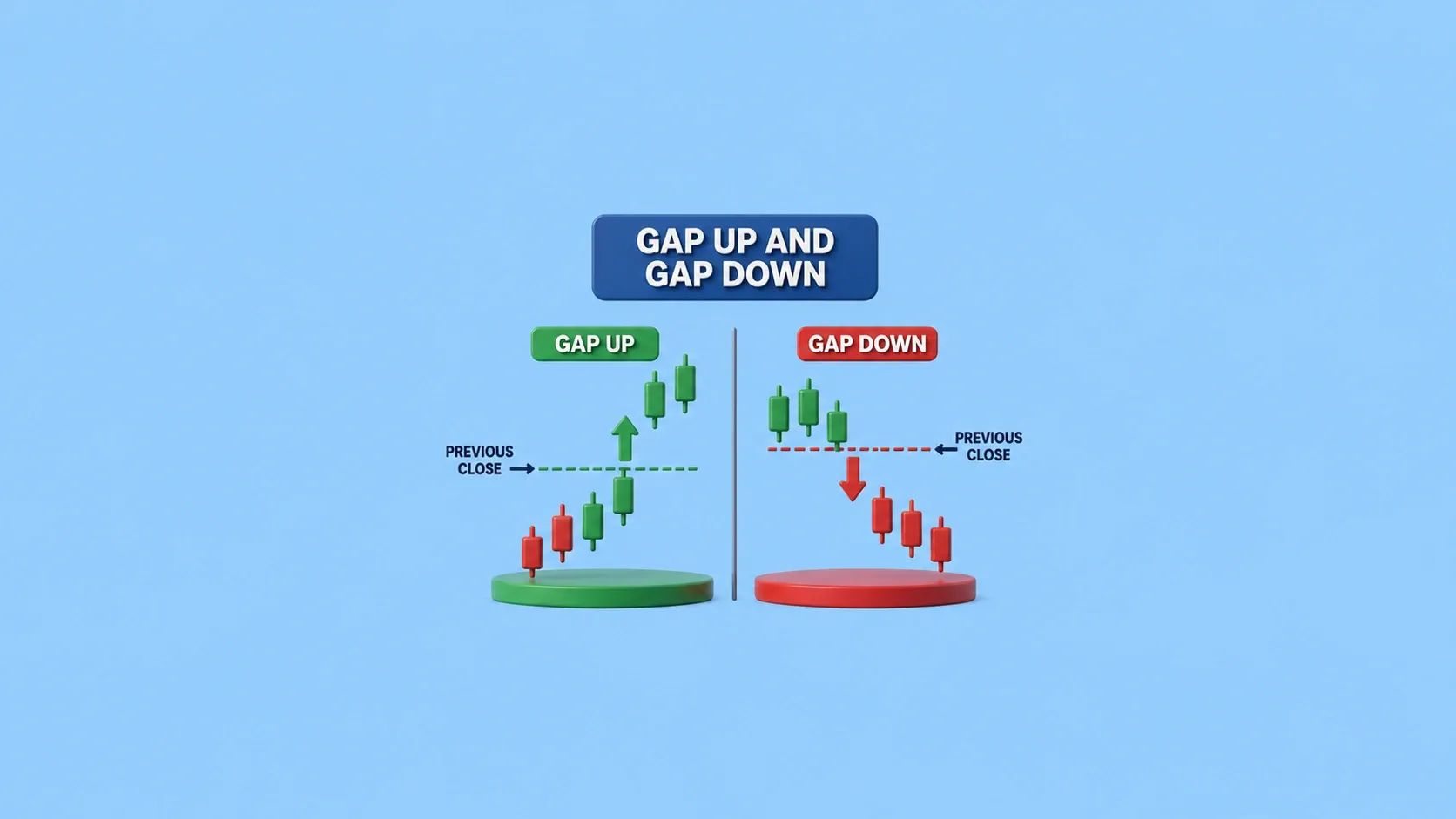

Have you ever opened your trading app and noticed that a stock or the Nifty 50 opened significantly higher or lower than its previous day's closing price? This price difference is known as a gap up and a gap down, and it often reflects a sudden change in market sentiment caused by overnight events. Whether you're an intraday trader or a beginner, understanding what gap up and gap down are can help you make better trading decisions. These price gaps are often triggered by overnight events such a

29 July 2026

Keeping an eye on the stock market throughout trading hours isn't always possible. But that doesn't mean you have to sit out until the next trading day to act on your investment decisions. This is where the After- Market Order (AMO) comes in, allowing you to place your trades even when the market is closed. In this blog, we'll break down what after-market orders are, how they work, their key characteristics, benefits and limitations, and the different types available to investors. What is An

29 July 2026

FII DII Data Today 29th July 2026 CATEGORY DATE BUY VALUE (₹ Crores) SELL VALUE (₹ Crores) NET VALUE (₹ Crores) DII 29-July-2026 16,187.74 15,136.81 1,050.93 FII 29-July-2026 16,352.31 13,472.38 2,879.93 What are FII and DII in the Stock Market Foreign Institutional Investors (FIIs) invest in the Indian stock market from international markets, while Domestic Institutional Investors (DIIs) include mutual funds and institutional bodies operating from India. fii dii data helps trac

28 July 2026

Made for Traders.

Trusted by Investors.

Download FinX — trade confidently, invest

smarter, track everything.

Table of Contents

- What is the meaning of Demat Account?

- History of Demat Accounts in India

- Features and Benefits of a Demat Account

- Demat Account Opening Documents

- How Does a Demat Account Work?

- Types of Demat Accounts in India

- Demat Account Number and DP ID

- CDSL vs NSDL Account Format

- Demat Account Charges

- Demat Account 2FA (Two Factor Authentication)

- Demat Glossary

- Conclusion

- FAQ