May 11, 2026

Bull Flag Pattern

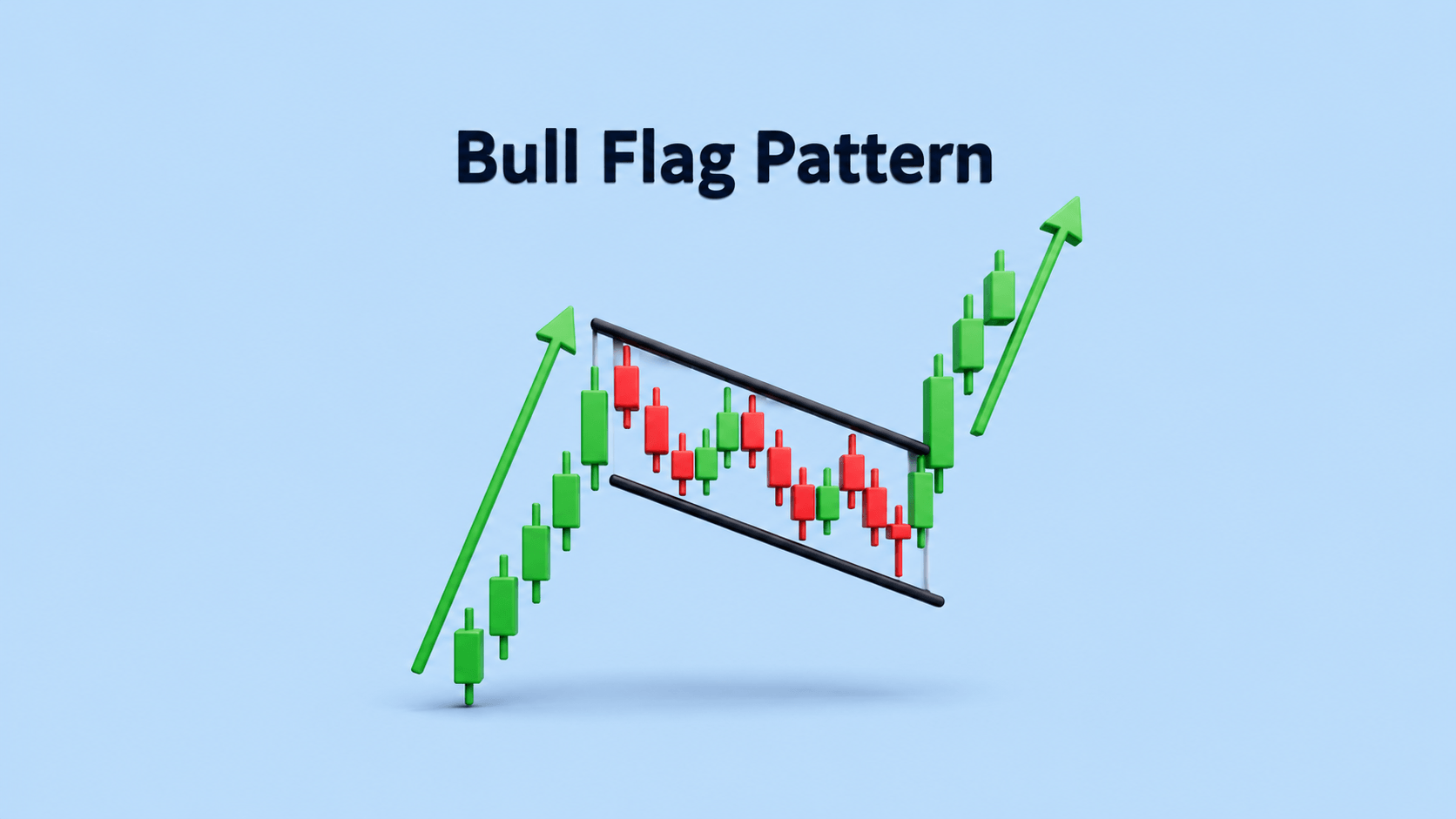

A bull flag pattern is a bullish chart pattern that signals trend continuation. This blog covers its meaning, formation, breakout strategy, and examples.

Explore our diverse investment options for your financial goals.

Get more value with our competitive pricing.

Plus ₹1,80,000+ worth of premium trading tools included free with Choice FinX.

Access ₹1,80,000+ worth of premium tools, expert research, and community-driven insights for free!

Real-time updates with instant impact analysis worth ₹36,000. Stay ahead of market movements.

Join India's active trader community. Share strategies and learn from experienced investors.

Get access to research calls from our Executive Director & Head of Technical Research.

Access professional hedged strategies worth ₹99,000. Risk-conscious trading made simple.

Get trading insights and recommendations for Intraday, F&O, and investments from our award-winning expert.

30.87%23.63%

30.87%23.63%Stay updated with the latest stock market news and articles.

Founded in 1992, Choice is a leading full-service stockbroker that combines innovative fintech solutions with personalised expertise to advance your investment goals.

Specialised services tailored to meet the unique needs of HNIs, businesses, and governments.

Expert guidance to optimise your business operations and strategy.

Comprehensive solutions for managing and growing your business wealth.

Strategic advice to help you make informed capital allocation decisions.

Championing the rights of individuals and businesses to financial freedom.

Experiences speak for themselves.