People with taxable income slabs often search for ways to save as much tax as possible. Using popular avenues like health insurance policies, life insurance, and HRA, it is possible to gain a much-needed reduction in tax liabilities. The entire process of financial planning to save tax is termed tax planning.

Tax planning is gaining more traction, with India’s personal income tax rate scheduled to touch 42.74% before the start of 2024. More salaried professionals are exploring tax saving options in form of tax exemptions and rebates to minimise the amount they pay annually.

But how much tax can you save? Read on as we delve deeper into what tax planning is and discuss the types, along with the options available to save tax.

Tax Planning: The Basics

Tax planning is a form of financial strategy to gain the maximum reduction on your tax slab. It promotes tax efficiency and helps decrease the incidence of tax. For effective tax planning, you can use all the provisions supplied by the Government of India in the Income Tax Act, 1961, and direct some amount to other avenues.

The budget for the fiscal year 2023-24 released by the Indian Government highlighted the emergence of two tax regimes - new and old. While the former has brought several benefits for the taxpayers, the old regime comprises exemptions and rebates. If you choose the new tax regime, you might not be able to claim certain reductions under the Income Tax Act of 1961.

Some of the benefits of tax planning are as follows:

- Reduces tax disputes

- Promotes economic stability

- Helps invest in avenues that secure your financial future

- Minimises tax liabilities in a given year

- Exemptions and rebates are governmental incentives to encourage a specific economical decision, like investing in life insurance policies.

Types of Tax Planning

Tax planning is broadly categorised into four groups, depending on the type of exemptions and rebates you choose to claim. Here are the four types:

Long-Term Tax Planning

In long-term tax planning, you invest in certain avenues throughout the financial year. You have to consistently follow this strategy to avail the maximum benefits at the end of the fiscal year.

For instance, systematic investment plans (SIPs) into public provident funds or ELSS mutual funds are considered tax-exempt. The only criterion is that you continue investing throughout the year to gain tax relief while slowly increasing your corpus.

Short-Term Tax Planning

The benefit of short-term tax planning is that you can deposit a lump sum at any point in the financial year to gain tax benefits. While it requires you to keep a significant amount ready, it is a good way if you have an erratic income or have defined your tax planning goals.

A good example is a medical insurance policy. You are only required to pay a premium once every year for most policies to be active, and this amount counts as a tax exemption.

Purposive Tax Planning

Although long-term and short-term planning is widely used and easy to understand, purposive tax planning requires significant financial planning. It is a plan of action in which you invest in tax-saving schemes that help you achieve long-term investment goals.

Permissive Tax Planning

Permissive tax planning helps people avail themselves of the maximum deductions under all relevant provisions of the Income Tax Act of 1961. It focuses on gaining tax benefits without accounting for your goal. So, if you are only looking to reduce tax liabilities and have no specific short-term or long-term aim, this is the perfect way to plan your taxes.

Exemptions and Rebates under the Old Tax Regime

The Income Tax Act of 1961 has various sections that emphasise tax breaks through other investment opportunities that are valuable for you. Some of the sections in the act and their benefits are as follows:

Section 80C

You can save a maximum of 46,500 under section 80C. Some of the avenues to achieve this are given below.

Equity-Linked Saving Scheme (ELSS): These mutual funds invest in equities in the stock market. ELSS is the only plan that offers tax benefits and requires you to lock in your amount for a minimum period of three years. However, ELSS has displayed promising performance over the years, with an average return of 4.34% across all fund houses in 2022.

Public Provident Fund (PPF): With an annually compounded interest rate, PPF offers one of the safest investment options if you want to gain tax benefits. It does not have a cap for minimum investment and is a feasible option for building long-term wealth at a relatively lower risk. The interest rate on PPF is 7.1% at the moment.

Unit Linked Insurance Plans (ULIP): These plans offer a life insurance policy to address the financial needs of your loved ones after your demise and provide an investment plan to help diversify your portfolio. ULIPs invest in the stock market, preventing the need for you to get personally invested in the space.

Section 80CC

It mainly deals with annuity pension plans. An annuity plan is a scheme where you deposit a lump sum and avail of a monthly pension after retirement. You can deposit this sum at once or use instalments to build your corpus. You can use the investments to claim a tax break under section 80CC of the Income Tax Act, 1961.

Section 80TTA

This section deals with the interest you accrue in your bank account or investments made in the local post office or cooperative society. It grants you a maximum deduction of Rs 10,000 for the interest gained in these avenues. However, section 80TTA does not apply to the interests of fixed deposits or corporate bonds.

Section 80GG

The deduction of house rent is the focal point of section 80GG. It states that if you do not receive an HRA from your employer, you can claim a deduction for the amount you pay to reside in a rental property. The only requisite is that you should not own a residential property in your place of employment.

Section 80E

If you or your family members have taken out an educational loan, you can claim a deduction for section 80E for 8 years from the start of the interest or until the loan amount is completely paid, whichever comes first.

Section 80D

Using section 80D, you can claim a deduction for the premium paid towards medical insurance every year. The premium can be for you, your spouse, your children or any other immediate dependents.

Summing Up

You can also claim deductions for other purposes, like donating to political parties or handling the medical expenditure of a disabled person. However, these are conditional and may not be valuable if you are looking for a strategic tax planning method.

According to your long-term financial goals, you can decide the ideal tax-saving avenues for you and plan your investments accordingly. Generally, it is a good idea to invest in policies and health insurance to safeguard your overall well-being while also gaining tax benefits.

So, get started on your journey today and reduce your tax liabilities for better economic stability in the future!

Related Blog

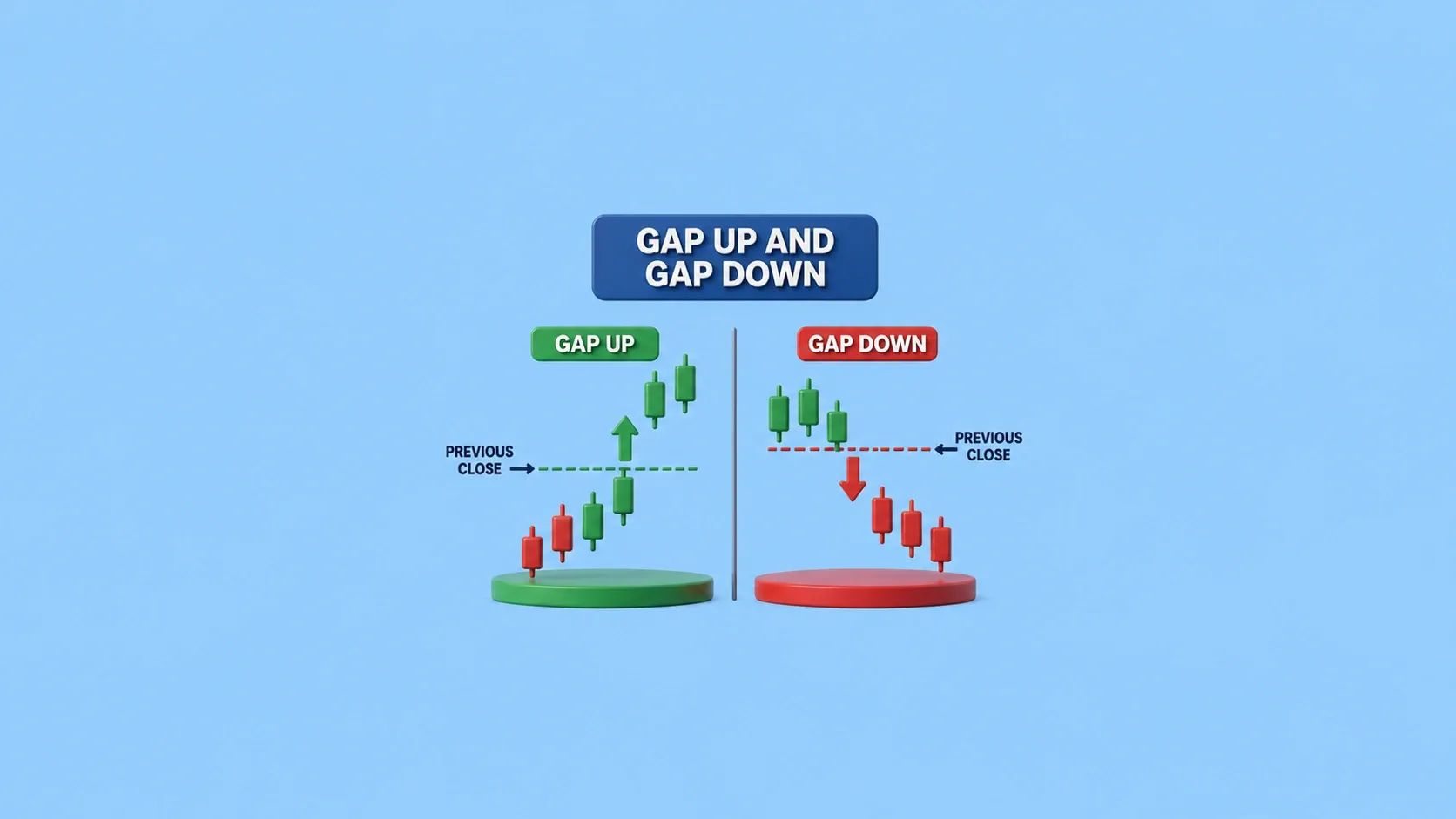

Have you ever opened your trading app and noticed that a stock or the Nifty 50 opened significantly higher or lower than its previous day's closing price? This price difference is known as a gap up and a gap down, and it often reflects a sudden change in market sentiment caused by overnight events. Whether you're an intraday trader or a beginner, understanding what gap up and gap down are can help you make better trading decisions. These price gaps are often triggered by overnight events such a

29 July 2026

Keeping an eye on the stock market throughout trading hours isn't always possible. But that doesn't mean you have to sit out until the next trading day to act on your investment decisions. This is where the After- Market Order (AMO) comes in, allowing you to place your trades even when the market is closed. In this blog, we'll break down what after-market orders are, how they work, their key characteristics, benefits and limitations, and the different types available to investors. What is An

29 July 2026

FII DII Data Today 29th July 2026 CATEGORY DATE BUY VALUE (₹ Crores) SELL VALUE (₹ Crores) NET VALUE (₹ Crores) DII 29-July-2026 16,187.74 15,136.81 1,050.93 FII 29-July-2026 16,352.31 13,472.38 2,879.93 What are FII and DII in the Stock Market Foreign Institutional Investors (FIIs) invest in the Indian stock market from international markets, while Domestic Institutional Investors (DIIs) include mutual funds and institutional bodies operating from India. fii dii data helps trac

28 July 2026

Made for Traders.

Trusted by Investors.

Download FinX — trade confidently, invest

smarter, track everything.