The Income Tax Department of India imposes taxes according to your income bracket. There have been a few changes in how this works, considering the recent announcement of Budget 2023.

Those aside, payment obligations still increase with higher annual salaries. This can amount to a significant number for those earning above 10 lakhs to 15 lakhs.

For those wondering about how to save tax on salary packages in that range, there are several available channels. While tax saving investments are the most commonly used examples, individuals can avail of multiple other components.

This article takes a deep dive into the very same. However, before getting into that, let’s establish the fundamentals first.

What are the New Income Tax Rates for the FY 2023-2024?

Before becoming familiar with the available tax saving options, it is crucial to know the revised rates under the new income tax regime. While there are additional conditions attached to the policy changes, the general outline for the tax slab for the FY 2023-2024 is as follows:

Income Category | Tax Rates |

Up to 3,00,000 INR | Nil |

Between 3,00,000 INR to 6,00,000 INR | 5% of total income exceeding 3,00,000 INR |

Between 6,00,000 INR to 9,00,000 INR | 10% of total income exceeding 6,00,000 INR |

Between 9,00,000 INR to 12,00,000 INR | 15% of total income exceeding 9,00,000 INR |

Between 12,00,000 INR to 15,00,000 INR | 20% of total income exceeding 12,00,000 INR |

Above 15,00,000 INR | 30% on total income exceeding 15,00,000 INR |

What are Some Common Tax Exemption Components & Deductibles?

Regardless of which tax slab category you fall under, your salary structure will consist of multiple components. Some of these are directly exempt from taxation, while other expenses are deductible.

As such, before establishing how to save tax on salary packages above 10,00,000 INR to 15,00,000 INR, you must determine your net taxable amount. This is calculated as follows:

- Gross Salary – Exempt Salary Components = Taxable Income

- Taxable Income – Deductions = Net Taxable Amount

To determine your salary structure, approach your HR department for details regarding the CTC or derive the information from your most recent pay stub.

Nonetheless, aside from minor variations, a typical salary structure will consist of the following:

Salary Component | Exemptions/Taxability |

Basic | No Exemptions/Fully Taxable |

Dearness Allowance | No Exemptions/Fully Taxable |

House Rent Allowance or HRA (Under Section 80GG) | Exempt up to 1,50,000 INR if specified in the salary structure (Up to 60,000 if not) |

Leave Travel Allowance (LTA) | Exemption under Section 10(5) for travel ticket expenses for up to 2 trips in 4 years |

Mobile & Internet Reimbursements | Exempt if said services are primarily for work/office purposes, with proof of payment or bills submitted |

Children’s Education & Hostel Allowance | Up to 4800 INR per child (Maximum of 2 children) |

Food Coupons | Up to 50 INR per meal (Maximum of 2 meals daily) Monthly amount: 100 x 26 (2600 INR) Annual amount: 2600 x 12 (31,200 INR) |

Standard Deduction | Up to 50,000 INR (Given to everyone without any restriction) |

Professional Tax | 2,400 INR in most cases (Varies across states) |

Apart from the tax exemption components, you can also attribute specific expenses as deductibles. This includes the following:

Deduction Component | Conditional Amount |

Premium Payments on Health Insurance Policies (Under Section 80D) | For one's self, spouse, or children: 25,000 INR (50,000 INR for those above 60 years of age) For parents: 25,000 INR (50,000 INR for those above 60 years of age) |

Education Loans (Under Section 80E) | Deduction of the loan’s interest amount for 8 years, starting from the period of repayment (For any loan taken to educate one's self, spouse, children, or legal ward) |

Charitable Donations (Under Section 80G) | 50% to 100% of the total amount |

Investments in Tax Saving Tools/Instruments (Under Section 80C) | Tax savings for up to 1,50,000 INR per year for investments in the following:

|

Treatment Expenses for Disabled Dependents (Under Section 80DD) | Tax relief on medical expenses of disabled dependents of up to the following:

|

Home Loan Payments | Up to 1,50,000 INR for the principal amount under Section 80C Up to 2,00,000 INR for the interest amount under Section 24B |

Maturity Proceeds for Life Insurance Policies | Exemptions for sums that are less than:

|

How to Save Tax for Salary Above 10 Lakhs

Now that you understand the various channels and tools at your disposal let’s look at one of the simplest ways to save tax in India. Consider the example below:

Person X has a gross annual salary of 10,00,000 INR. Under the exempted components, this will include elements such as:

Exemptions | Amount |

HRA | 1,50,000 INR |

LTA | 40,000 INR |

Mobile & Internet Reimbursements | 24,000 INR |

Children’s Education & Hostel Allowance | 9800 INR |

Food Coupons | 31,200 INR |

Standard Deduction | 50,000 INR |

Professional Tax | 2400 INR |

Upon calculation, Person X’s taxable income will amount to 6,92,600 INR. Subsequently, they can make deductions in the following categories:

Deductions | Amount |

80C (Tax Saving Instruments) | 1,50,000 INR |

80D (Health Insurance Policy Payments) | 50,000 INR |

80E (Education Loans) | 25,000 INR |

This would bring the net taxable amount to 4,67,600 INR. Now, considering that the tax slab for the income category of 3,00,000 INR to 6,00,000 INR is 5%, that would mean a tax of merely 23,380 INR. However, since Budget 2023 includes a tax rebate for up to 7,00,000 INR, the total payable amount would essentially be nil.

There are similar tax saving options for salaried employees with annual packages of up to 15 lakhs. While the rebate will not nullify the tax entirely, the amount would still be significantly less than the gross value.

In addition, it is critical to note that, unless specifically opted for, all individuals will be taxed under the new regime. Thus, it is advisable to avail of the maximum number of tax deductions. This is relatively easy to achieve with the help of a Certified Public Accountant (CPA) or a licensed tax preparer.

Wrapping Up

Now that you understand how to save tax on salary above 10 or 15 lakhs. It is crucial to remember that government taxation policies tend to change every year.

As such, it would be best to keep track of the latest updates and recent announcements from the official channels. This will help you plan your tax-saving strategy while eliminating potential liabilities.

It also helps to leverage as many tax-free investments as possible, including EPFs, PPFs, and insurance premium payments. Doing so would allow you to make sizable deductions from your taxable income, resulting in a lower net tax amount.

Related Blog

Many investors begin their Mutual fund journey to grow their wealth, but terms like open-end funds and closed-end funds can often be confusing. While both are regulated by SEBI, they differ in how you invest, redeem your money, and the level of flexibility they offer. Choosing the right one depends on your financial goals, investment horizon, and liquidity needs. In this article, we'll explain what an open-ended mutual fund is, what a closed-end fund is, the difference between open-ended and cl

31 July 2026

If you have ever browsed through IPO websites, you must have seen sections mentioning “Mainboard IPOs” and “SME IPOs”. They are both termed IPOs, but what is the difference between them? Understanding this difference matters, especially if you are new to investing in IPOs. In this blog, we will discuss what a Mainboard IPO and an SME IPO actually are, how they differ, the key differences in their risk characteristics and how you can apply to one through Choice. What Is a Mainboard IPO? A Mai

31 July 2026

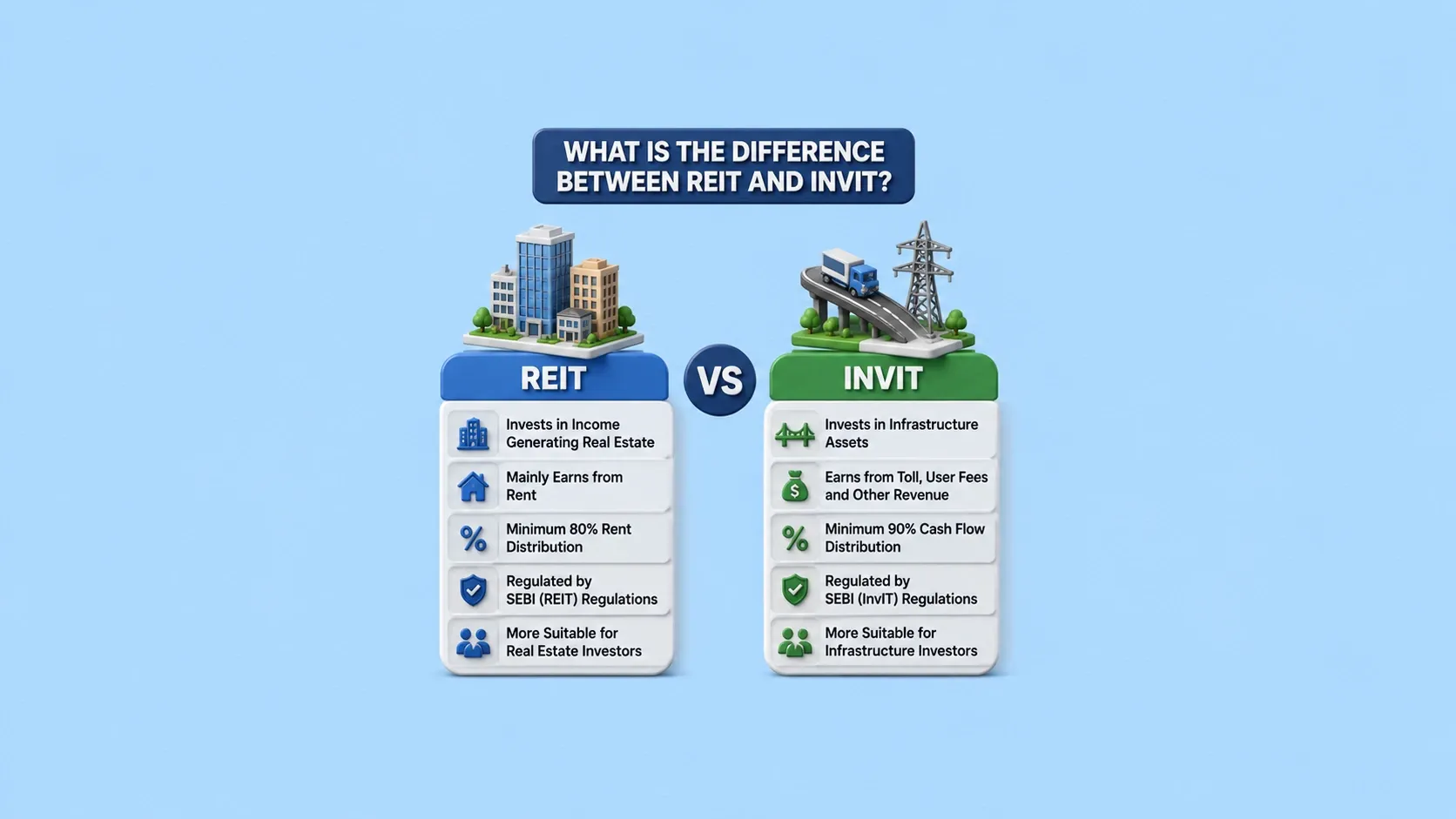

If you're looking to diversify beyond stocks, mutual funds and fixed deposits, REITs and InvITs are two investment options worth understanding. They both allow you to invest in large-scale assets such as Real Estate and infrastructure, without buying them directly. While they might have some similarity, they invest in different types of assets, carry different risk profiles and are suited for different kinds of investors. In this blog, we will learn what each instrument is, how they compare to

31 July 2026

Made for Traders.

Trusted by Investors.

Download FinX — trade confidently, invest

smarter, track everything.