The Reserve Bank of India delivered a bold move on June 6, 2025, cutting the repo rate by 50 basis points to 5.50% — double what most analysts expected. This marks the third consecutive rate cut this year, bringing the total reduction to 100 basis points since February 2025.

RBI's Strategic Policy Shift

During the Monetary Policy Committee meeting, RBI Governor Sanjay Malhotra announced the jumbo 50 basis points cut, citing the need to spur economic growth as inflation has come down below the lower RBI band of 4 per cent. The central bank also shifted its policy stance from "accommodative" to "neutral," signalling a more data-driven approach going forward.

Along with the repo rate cut, other key rates were adjusted:

Standing Deposit Facility (SDF) rate: 5.25%

Marginal Standing Facility (MSF) rate and Bank Rate: 5.75%

Cash Reserve Ratio (CRR): Cut by 100 basis points to 3%

Why This Rate Cut Matters

The RBI cut the repo rate by a higher-than-expected 50 basis points to prop up growth, which has slowed to a four-year low of 6.5 per cent in FY25. This aggressive move demonstrates the central bank's commitment to supporting economic expansion while maintaining price stability.

The CRR reduction will inject approximately ₹2.5 lakh crore into the banking system, enhancing liquidity and supporting credit growth across sectors.

Immediate Market Response

Financial markets responded positively to the announcement:

Nifty 50 crossed the 24,900 mark

BSE Sensex rose to 82,022 points

Banking stocks showed mixed reactions due to margin compression concerns

Rate-sensitive sectors like real estate and housing finance companies surged up to 4-5%

Impact on Different Sectors

Banking Sector

While the rate cut reduces banks' borrowing costs, it creates short-term pressure on net interest margins. Private banks with higher retail exposure face potential income compression, while public sector banks may benefit from increased loan demand.

Real Estate Boom

The real estate sector stands to gain significantly from this move. Home loan EMIs will decrease for existing floating rate borrowers, while new borrowers can access some of the lowest interest rates in recent years. This is particularly beneficial for the affordable and mid-income housing segments that have struggled in recent years.

Consumer Spending

Lower borrowing costs are expected to boost consumer spending on automobiles, consumer durables, and other big-ticket items. The move provides much-needed support to urban consumption, which has shown weakness in previous quarters.

What Industry Leaders Say

Market experts view this as a growth-focused decision that balances economic expansion with inflation control. The move is expected to stimulate domestic demand, support MSMEs, and encourage private capital expenditure.

Real estate industry leaders particularly welcome the decision, noting that it could revive the lower and mid-value housing segments that have been underperforming compared to premium properties.

CPI Inflation Outlook

The RBI revised its CPI inflation projection for FY 2025-26 downward to 3.7% from the earlier estimate of 4.0%. Quarterly projections show:

Q1: 2.9%

Q2: 3.4%

Q3: 3.9%

Q4: 4.4%

What This Means for Borrowers

Home loan borrowers with floating rate loans will see immediate relief in their EMIs. New borrowers can take advantage of reduced interest rates, making property purchases more affordable. Similarly, auto loans and personal loans are expected to become cheaper.

Looking Ahead

The shift to a "neutral" stance suggests the RBI will adopt a more cautious, data-dependent approach for future rate decisions. Global uncertainties, including trade tensions and geopolitical factors, will influence the central bank's policy direction.

The RBI has maintained its GDP growth projection at 6.5% for FY 2025-26, indicating confidence in the economy's resilience despite global headwinds.

Bottom Line

The RBI's 50 basis points repo rate cut represents a significant stimulus for the Indian economy. While banks may face short-term margin pressures, the overall impact is positive for borrowers, investors, and economic growth. The move signals the central bank's commitment to supporting domestic demand and ensuring adequate liquidity in the financial system.

For investors and borrowers, this creates opportunities across multiple sectors, particularly in real estate, consumer goods, and rate-sensitive industries. The key now is monitoring how effectively banks transmit these rate cuts to end consumers and whether the stimulus translates into sustained economic growth.

Disclaimer: This information is for educational purposes only and should not be considered as investment advice. Please consult with a qualified financial advisor before making any investment decisions.

Related Blog

Many investors begin their Mutual fund journey to grow their wealth, but terms like open-end funds and closed-end funds can often be confusing. While both are regulated by SEBI, they differ in how you invest, redeem your money, and the level of flexibility they offer. Choosing the right one depends on your financial goals, investment horizon, and liquidity needs. In this article, we'll explain what an open-ended mutual fund is, what a closed-end fund is, the difference between open-ended and cl

31 July 2026

If you have ever browsed through IPO websites, you must have seen sections mentioning “Mainboard IPOs” and “SME IPOs”. They are both termed IPOs, but what is the difference between them? Understanding this difference matters, especially if you are new to investing in IPOs. In this blog, we will discuss what a Mainboard IPO and an SME IPO actually are, how they differ, the key differences in their risk characteristics and how you can apply to one through Choice. What Is a Mainboard IPO? A Mai

31 July 2026

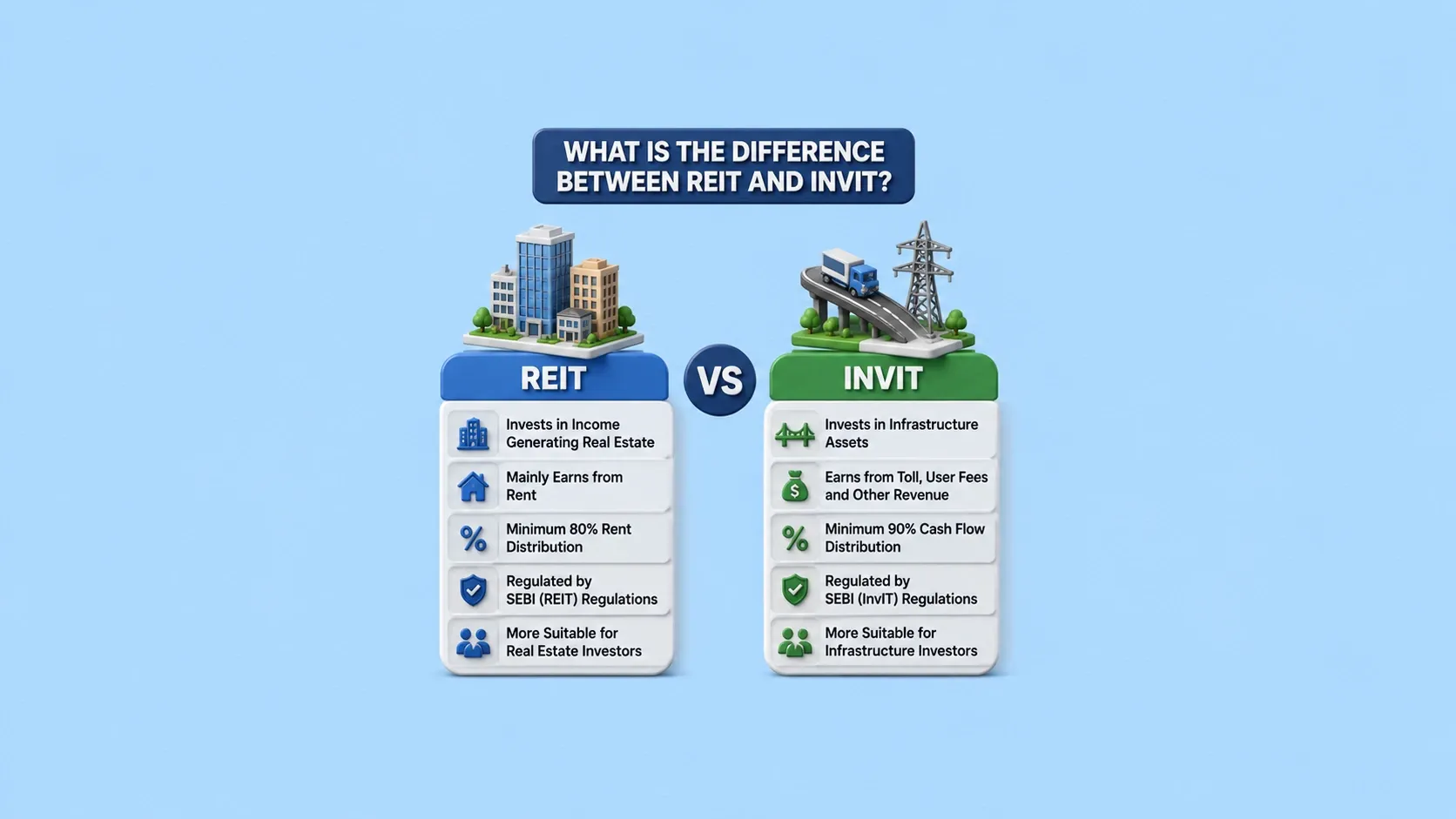

If you're looking to diversify beyond stocks, mutual funds and fixed deposits, REITs and InvITs are two investment options worth understanding. They both allow you to invest in large-scale assets such as Real Estate and infrastructure, without buying them directly. While they might have some similarity, they invest in different types of assets, carry different risk profiles and are suited for different kinds of investors. In this blog, we will learn what each instrument is, how they compare to

31 July 2026

Made for Traders.

Trusted by Investors.

Download FinX — trade confidently, invest

smarter, track everything.