The world of investments can be exciting, but for sure, it does have a lot of pitfalls. Understanding how your gains are taxed is crucial to calculate your real returns. If your portfolio does grow over time and you are considering selling some of these assets, whether such gains are to be regarded as long-term or short-term will hugely affect your tax liabilities. Having insights into how these sorts of gains are taxed can make a huge difference in your investment strategy and overall returns.

In this blog, we'll outline the critical distinctions between long-term and short-term capital gains, examining how each is taxed and what that might mean for your financial plan.

What Are Capital Assets?

Any valuable resource an individual or business might sell following its acquisition and utilisation for a period could be considered a capital asset. Capital assets are categorised as follows:

- Tangible Assets: These are physical items, such as real estate, vehicles, and machinery.

- Intangible Assets: Non-physical assets include stock, bonds, intellectual property, and goodwill.

In the case of a sale of capital assets, any profit or loss derived from it is subject to tax, known as capital gains tax, as per the Income Tax Act, 1961. The applicability of the tax rate depends upon whether the asset has been held for the long term or the short term.

What are Long-Term Capital Gains?

LTCG Full form is long-term capital gain. It means profits made from the sale of assets held beyond 12 months. The tax incurred on such gains is called LTCG tax.

In India, LTCG from listed equity shares and equity mutual funds is exempt up to Rs. 1 lakh in a financial year. Gains above this limit are taxed at the rate of 10% without indexation benefits. For other assets like real estate or gold, LTCG is taxable at 20% with indexation benefits that inflate the purchase price for the inflationary effect to reduce the taxable gain.

LTCG Calculation

The general formula to calculate LTCG is,

LTCG = Selling Price of Asset - Cost of Acquisition (adjusted for indexation, if applicable) - Allowable Expenses

where,

Selling Price of Asset: The total amount received for the sale price after deducting any transaction fees.

Cost of Acquisition: The asset's purchase price, adjusted for inflation using an indexation factor in the case of debt mutual funds and physical gold held before April 1, 2023. Indexation is not applicable as of January 2024 for equity shares. Acquisition expenses include stamp duty or registration charges paid.

Allowable Expenses: Expenses only accrued in direct relation to the sale of items, such as brokerage fees, advertising, and transfer charges.

What are Short-Term Capital Gains?

Short-term capital gain (STCG) is the gain that arises from the transfer of a short-term capital asset. STCG is considered when the assets are held for less than 12 months. The corresponding tax rate is known as the STCG tax.

For listed equity shares and equity mutual funds in India, STCG comes under the ambit of taxation at the rate of 15%. STCG, in the case of other assets like real estate or gold, is taxed at applicable income tax slab rates. That simply means these gains are taxed as your regular income, with rates as high as 30% plus applicable surcharges and cess.

STCG Calculation

The simple formula to calculate STCG is,

STCG = Selling Price of Asset - Cost of Acquisition - Allowable Expenses

where

Selling Price of Asset: The total amount received from the sale, including any brokerage or transaction fees.

Cost of Acquisition: The asset's purchase price plus any incidental expenses, such as stamp duty or registration fees.

Allowable Expenses: Costs incurred directly related to the sale, including brokerage fees, advertising expenses, and transfer charges.

Difference Between LTCG and STCG

The table below shows the differences between STCG and LTCG:

| Aspect | LTCG (Long-Term Capital Gains) | STCG (Short-Term Capital Gains) |

|---|---|---|

| Holding Period | More than 12 months | Less than 12 months |

| Tax Rate | 10% for equity (above Rs. 1 lakh); 20% for other assets with indexation benefits | 15% for equity; Slab rates for other assets |

| Tax Benefit | Tax-free up to Rs. 1 lakh for equity; 20% with indexation for other assets | No special exemptions or reductions |

| Investment Horizon | Long-term, typically for growth | Short-term, usually for quick gains |

| Indexation Benefit | Available for other assets (not for equity), reduces the taxable gain | Not available |

LTCG Vs STCG — Which is Better?

LTCG, more often than not, has particular tax advantages and is suitable for long-term investments. Conversely, STCG can work with an active trading strategy. Being aware of their respective tax provisions will aid you in better investment decisions and enable the proper optimisation of your taxes.

The choice between LTCG and STCG depends on an individual's investment strategy and tax considerations:

- LTCG: Generally offers tax benefits to long-term investors. In India, the LTCG on equity investment is exempt up to Rs 1 lakh per financial year, and other assets are entitled to a concessional rate of taxation at 20% with indexation. This will make LTCG a promising avenue for long-term growth-oriented investors who can avail themselves of the benefits of reduced taxation rates and adjustments for inflation.

- STCG: This would be ideal for investors who trade more frequently and look forward to making short-term gains. STCG is taxed at 15% in the case of equity investments, which is higher compared to the LTCG rate. For the rest, it is at the slab rates, which might be much higher since it would depend on your income level. It will be suitable for those who manage to capitalise on the movement in the market in the short term, but at the same time, it has a relatively higher tax burden.

Long-Term Vs Short-Term Capital Gains For Asset Classes Based on Budget 2024

The table below lists the LTCG and STCG for different types of asset classes:

| Asset Class | Holding Period for Classification as LTCG | Short-Term Capital Gains Tax | Long-Term Capital Gains Tax |

|---|---|---|---|

| Listed Equity Shares / Units of Equity-Oriented MFs / Business Trusts (REITs / InVITs) | >12 months | 12.5% on gains exceeding Rs. 1,25,000 | 20% |

| Unlisted Shares | >24 months | Applicable tax slab | 12.5% without indexation |

| Listed Securities (Other than units) or Zero-Coupon Bonds | >12 months | Applicable tax slab | 12.5% without indexation |

| Unlisted Debentures and Bonds | >24 months | Applicable tax slab | Applicable tax slab |

| Market-Linked Debentures and Debt Mutual Funds | >24 months | Applicable tax slab | Applicable tax slab |

| Land, Building | >24 months | Applicable tax slab | 12.5% without indexation |

| Physical Gold | >24 months | Applicable tax slab | 12.5% without indexation |

| Gold ETF | >12 months | Applicable tax slab | 12.5% without indexation |

| Sovereign Gold Bond (SGB) | >12 months | Applicable tax slab | 12.5% without indexation |

Exemption from Capital Gains Tax: How to Avail?

Following are a few ways to enjoy capital gains exemption:

- Buy a New House: If the amount gained as capital gains is invested in purchasing a new house, it will have no tax to be paid. Make sure that you have purchased the new home within the same year before you file your income tax.

- Investment in Specific Bonds: Invest your capital gains in the bonds issued by Rural Electrification Corporation Limited or National Highway Authority of India with a lock-in period of at least 3 years. Keep in mind that the maximum limit for investment in these bonds is Rs 50 lakh in a financial year.

- Investment in Capital Gains Account Scheme (CGAS): If you do not want to invest in a property right away, then deposit the capital gains in CGAS with any public sector bank. The amount needs to stay in the account for 2 to 3 years. By the end of the term, ensure the money is utilised to buy property, or the gains shall be taxable. In the case of ready-made property, you have to invest in 2 years, while for under-construction property, this period is 3 years.

- Delayed Property Handover: If a builder cannot give you the property ownership in 3 years, you shall be exempted from paying any tax.

- Stamp Duty and Registration Fees: These costs are considered for capital gains calculation.

Tax Loss Harvesting Strategy to Reduce Capital Gains Tax

Tax-loss harvesting is a method of realising losses by selling some investments to set off against capital gains, reducing the amount of taxes the investor has to pay. By turning in a loss, you will reduce the amount of taxes you pay on the gains coming from other investments through the strategic realisation of losses. Here's how you can put this into practice:

Suppose you have invested Rs. 4 lakh in an Equity Mutual Fund, for which the value comes down to Rs. 3 lakh as of March 2023, and accordingly, a long-term capital loss of Rs 1 lakh is considered. In the same year, you make a long-term capital gain of Rs 1.5 lakh from some other investments.

| Details | Amount |

|---|---|

| Initial Investment | Rs. 4 lakh |

| Current Investment Value | Rs. 3 lakh |

| Long-Term Capital Loss | Rs. 1 lakh |

| Long-Term Capital Gains (Same Year) | Rs. 1.5 lakh |

| Taxable Long-Term Capital Gains (Without Offsetting) | Rs. 1.5 lakh |

| Long-Term Capital Loss Applied | Rs. 1 lakh |

| Net Taxable Long-Term Capital Gains | Rs. 50,000 |

| Total Capital Gains Tax Payable (at 10%) | Rs. 5,000 |

Conclusion

Effectively managing your capital gains requires much more than just understanding the tax rates. It requires a strategic way in which you can better optimise your investment outcomes. You will be able to make the best decisions concerning your financial goals and tax strategies by making a distinction between long-term and short-term capital gains.

Keep in mind that it is not about trying to comply with taxes but instead how you can use such taxes to your advantage. You can then manage your investments with this in mind in such a way that returns are maximised and tax liabilities are kept to a minimum.

Interested in investing in saving capital gains while maximising your profits? Explore the Choice platform for expert guidance and tips on maximising your investment benefits.

FAQ

What are STCG and LTCG Tax Rates?

After Budget 2024, short-term capital gains (STCG) from equity investments are taxed at 20%, while other assets are taxed based on their applicable rates. Additionally, long-term capital gains (LTCG) from all types of capital assets are now taxed at 12.5%, with an exemption for up to Rs 1.25 lakh per financial year.

Related Blog

Many investors begin their Mutual fund journey to grow their wealth, but terms like open-end funds and closed-end funds can often be confusing. While both are regulated by SEBI, they differ in how you invest, redeem your money, and the level of flexibility they offer. Choosing the right one depends on your financial goals, investment horizon, and liquidity needs. In this article, we'll explain what an open-ended mutual fund is, what a closed-end fund is, the difference between open-ended and cl

31 July 2026

If you have ever browsed through IPO websites, you must have seen sections mentioning “Mainboard IPOs” and “SME IPOs”. They are both termed IPOs, but what is the difference between them? Understanding this difference matters, especially if you are new to investing in IPOs. In this blog, we will discuss what a Mainboard IPO and an SME IPO actually are, how they differ, the key differences in their risk characteristics and how you can apply to one through Choice. What Is a Mainboard IPO? A Mai

31 July 2026

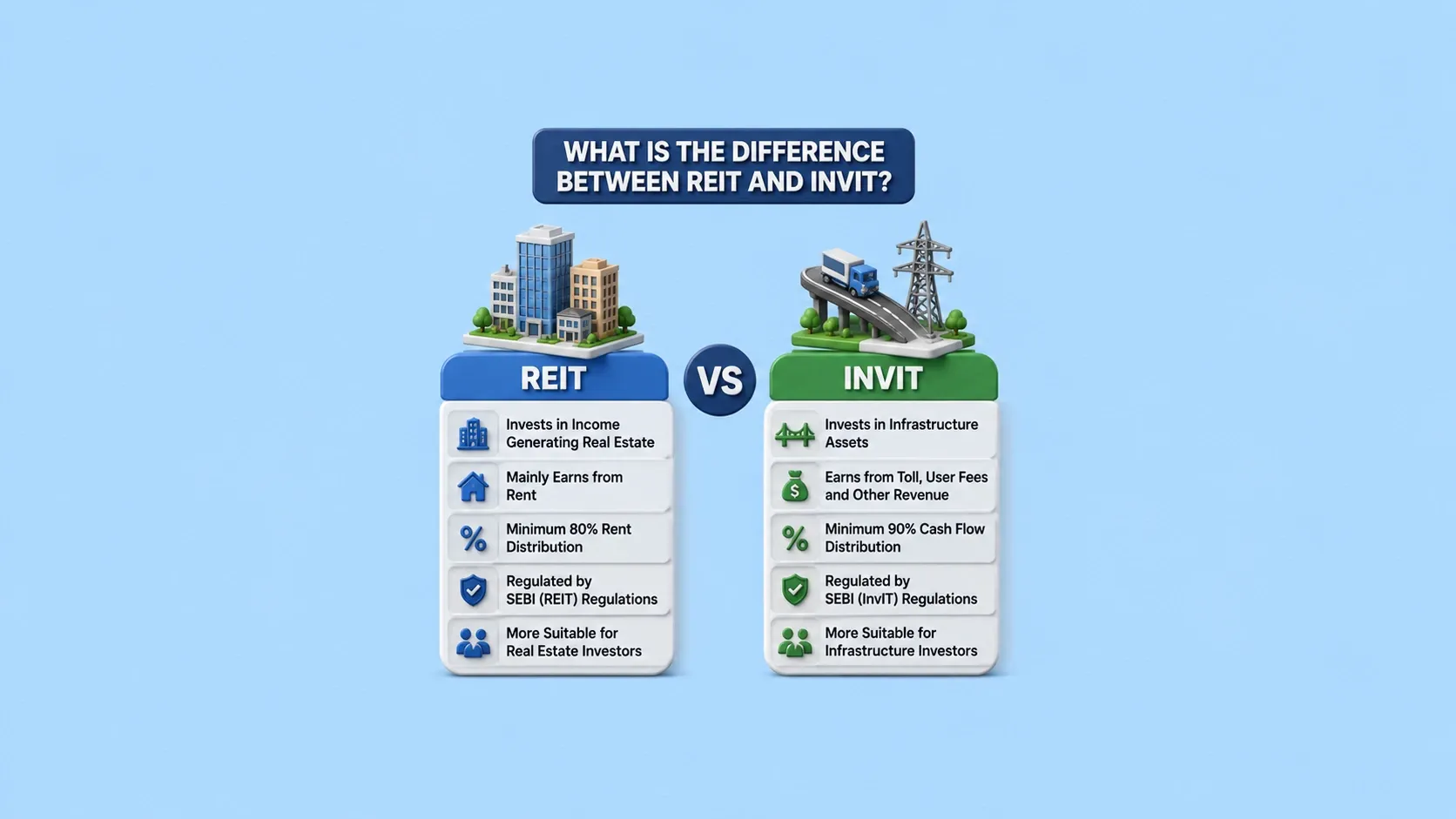

If you're looking to diversify beyond stocks, mutual funds and fixed deposits, REITs and InvITs are two investment options worth understanding. They both allow you to invest in large-scale assets such as Real Estate and infrastructure, without buying them directly. While they might have some similarity, they invest in different types of assets, carry different risk profiles and are suited for different kinds of investors. In this blog, we will learn what each instrument is, how they compare to

31 July 2026

Made for Traders.

Trusted by Investors.

Download FinX — trade confidently, invest

smarter, track everything.

Table of Contents

- What Are Capital Assets?

- What are Long-Term Capital Gains?

- What are Short-Term Capital Gains?

- Difference Between LTCG and STCG

- LTCG Vs STCG — Which is Better?

- Long-Term Vs Short-Term Capital Gains For Asset Classes Based on Budget 2024

- Exemption from Capital Gains Tax: How to Avail?

- Tax Loss Harvesting Strategy to Reduce Capital Gains Tax

- Conclusion

- FAQ