Financial planning has become much more complicated and intricate. Amassing your wealth while finding ways to manage your taxes efficiently is crucial. Most people are looking for ways that not only avail them of tax relief but also entail high returns on investments. Several schemes aimed at saving taxes go hand-in-hand with serving these dual purposes, proving worthy of being availed.

In this blog, we will introduce different tax-saving schemes and explain how each works and what kind of benefit each will provide. From conventional saving schemes to new forms of investment, we will discuss how such schemes serve the dual purpose of reducing your tax burden and enhancing financial growth.

Tax Saving Schemes in India: An Overview

Taxation planning forms an integral part of financial planning. If rightly availed of, tax-saving schemes can promptly and effectively translate savings on your total taxable income into substantial savings. Tax-saving schemes are financial products or investment options aimed at reducing your taxable income, hence reducing the amount of tax payable. This is important in financial planning, as it works with managing one's taxable income against building up wealth.

When used effectively, this will keep you on the radar for deductions, exemptions, and rebates toward an efficient way of upgrading financial health.

Top Tax Saving Schemes in India

Let’s explore the different ways to save taxes:

Section 80C

Section 80C of the Income Tax Act allows taxpayers to claim deductions up to ₹1.5 lakh per annum on specific investments and expenditures. This section is highly popular due to its wide range of eligible investment options.

| Investment | Description | Lock-in Period | Pros | Cons |

|---|---|---|---|---|

| Public Provident Fund (PPF) | Government-backed savings scheme with tax-free interest and returns | 15 years | Safe investment, tax-free returns, government-backed, long-term savings avenue | Long lock-in period, limited liquidity |

| Equity-Linked Savings Scheme (ELSS) | Mutual funds investing primarily in equities, offering tax benefits under Section 80C | 3 years | Potential for higher returns due to equity exposure and shorter lock-in period compared to PPF | Returns are subject to market fluctuations and risks |

| National Savings Certificate (NSC) | Fixed-income investment with guaranteed returns and a 5-year tenure | 5 years | Guaranteed returns, low risk | Lower liquidity, lower returns compared to equities |

| Tax-Saving Fixed Deposit (FD) | Fixed deposit with tax benefits under Section 80C and a 5-year lock-in | 5 years | Fixed returns are easy to understand and manage | Lower returns compared to equity-linked options, interest earned is taxable |

Section 80D

This section provides a deduction for the premium paid upon health insurance policy coverage for self spouse, children and parents.

- Pros: This deduction reduces individuals' taxable income and covers them for medical expenses. One can get up to ₹ 25,000 if they are below 60 years old and up to ₹ 50,000 in the case of a senior citizen.

- Cons: It requires one to pay the premium annually to avail of the deduction, which, therefore, could be a certain recurring financial burden.

Section 24(b)

This section permits up to ₹2 lakh deduction annually on the interest paid on home loans toward self-occupied properties.

- Pros: Good tax relief is provided to homebuyers; it decreases the effective cost of borrowing.

- Cons: Applies only when the property is kept for self-occupation and is not let out. The benefit is capped at ₹2 lakh annually.

Section 10(14)

House Rent Allowance: This is the allowance provided to employees by the employer to meet house rent expenses. This section allows deduction on income tax related to HRA received.

- Pros: Limits the taxable income of employees who get rented accommodations. The exemption is based on the rent paid, salary, and location of the place on rent.

- Cons: Exemption depends on actual rent paid and other factors like the employee's salary and HRA salary component.

Section 80E

This section provides interest deductions paid on loans taken for higher education. This can be availed on loans taken to educate yourself, your spouse, or your children.

- Pros: Helps manage the financial burden of education loans and provides tax relief for interest payments.

- Cons: Applies only to loans taken for higher education, not for other education expenses.

National Pension System (NPS)

NPS is an optional retirement savings scheme wherein the government offers tax exemption under section 80CCD 1B of ₹ 50,000 over and above ₹ 1.5 lakh limit for section 80C. NPS is meant to provide a regular pension post-retirement.

- Pros: Additional tax benefits, flexibility in contributions, and encouragement of long-term savings for retirement.

- Cons: The returns are subject to market risks. Withdrawals before retirement come with some limitations.

Tax Saving Schemes Other than 80C

Apart from Section 80C, different investment options are available that help you save tax in different ways. These are given below:

| Investment | Overview | Pros | Cons |

|---|---|---|---|

| Tax-Free Bonds | Issued by government-backed entities like IRFC and NABARD. Interest is tax-exempt. | Provides tax-free interest income, stable returns, and lower risk. | Generally offers lower returns compared to equity-based investments. |

| Public Provident Fund (PPF) | Long-term savings scheme with tax-free interest and returns. Government-backed. | Safe investment, tax-free returns, government-backed, long-term savings opportunity. | A 15-year lock-in period may not suit those needing quicker access to funds. |

| Fixed Deposits with Tax Benefit | Fixed deposits with a 5-year lock-in period offering tax benefits under Section 80C. | Fixed returns with tax benefits, easy to understand and manage. | Lower returns compared to market-linked instruments, interest earned is taxable. |

| Equity-Linked Savings Scheme (ELSS) | Mutual funds investing primarily in equities with tax benefits under Section 80C. | Potential for higher returns due to equity exposure and shorter lock-in period compared to other options. | Subject to market risks and fluctuations, which can impact returns. |

Tax Saving Investment Options for Salaried Individuals

Salaried individuals are provided with a set of specific tax-saving options, which, at times, can be designed and moulded according to their income structure. Some of the important schemes include:

- Health Insurance: Provides rebates for premiums that are paid on health insurance, whereby it reduces taxable income, and in return, it covers medical expenses.

- HRA: Provides an exemption in the rent paid that benefits people staying in rented accommodations.

- NPS: Facility to avail an additional tax-saving retirement planning option, contribution to which can be made as per one's capacity.

100% Tax-Free Investments

Here are four tax-saving investment options that help reduce your income tax and provide tax-free returns. Remember, these benefits apply exclusively to those who choose the old tax regime.

| Investment | Description | Tax Benefits |

|---|---|---|

| Public Provident Fund (PPF) | Invest under Section 80C to reduce taxable income. Offers tax-free interest and returns. | Tax-free interest and returns |

| Sukanya Samriddhi Yojana (SSY) | A deposit scheme for girl children under the "Beti Bachao, Beti Padhao" initiative. Provides tax benefits for education or marriage expenses. | Tax-free on investment, interest, and maturity amount (EEE status) |

| Employees Provident Fund (EPF) | Mandated contribution of 12% of salary from employees, with matching employer contribution. Contributions are eligible for deduction under Section 80C. | Tax-free interest and maturity amount; deductible contributions under Section 80C |

| Voluntary Provident Fund (VPF) | Allows employees to contribute more than the mandated 12% towards EPF. Contributions are eligible for deduction under Section 80C. | Tax-free interest and maturity amount; deductible contributions under Section 80C |

Comparison of Tax Savings Investment Options

Below is an overview of the different types of tax-saving investment options:

| Scheme | Tax Benefit | Lock-in Period | Risk-Reward | Investor Suitability |

|---|---|---|---|---|

| PPF | Tax-free returns | 15 years | Low risk, moderate reward | Suitable for risk-averse investors looking for a secure, long-term investment with guaranteed returns. |

| ELSS | Tax deduction | 3 years | High-risk, high reward | Suitable for investors with a higher risk tolerance seeking potentially higher returns and who can lock in their investment for 3 years. |

| NSC | Guaranteed returns | 5 years | Low-risk, fixed reward | Suitable for conservative investors who prefer guaranteed returns and a moderate lock-in period. |

| Tax-Saving FD | Tax deduction | 5 years | Low-risk, fixed reward | Suitable for risk-averse investors looking for guaranteed returns with a fixed investment period. |

| NPS | Up to ₹50,000 | Retirement age | Moderate risk, long-term reward | Suitable for individuals planning for retirement with a long-term investment horizon and who can handle moderate risk. |

Latest Income Tax Slabs and Rates - FY 2025-26 | AY 2026-27

Under the prevailing tax regime, the new tax regime is the default for the taxpayers, whereas those remaining under the old tax regime have to make a particular choice when filing their taxes. It is an option available every year for those who do not have business income. Regarding assessments with business income, the option between tax regimes is more limited.

They have to continue with the old tax regime so that continuity remains intact, and they only have a one-time option to revert to the new tax regime if they choose the latter initially. The idea is to have this setup, making the new tax regime the default while still allowing flexibility for those who want to continue with the benefits of the old regime.

New Tax Regime Changes

The new income tax slabs under the new tax regime, effective from April 1, 2024, have been updated. The changes, announced in July 2024, adjust two tax slabs:

| Income Range | Previous Rate | New Rate |

|---|---|---|

| ₹3 lakh - ₹6 lakh | 10% | 5% |

| ₹6 lakh - ₹9 lakh | 15% | 10% |

Updated tax slabs according to the new tax regime:

| Income Range | Tax Rate |

|---|---|

| ₹0 - ₹3,00,000 | 0% |

| ₹3,00,001 - ₹7,00,000 | 5% |

| ₹7,00,001 - ₹10,00,000 | 10% |

| ₹10,00,001 - ₹12,00,000 | 15% |

| ₹12,00,001 - ₹15,00,000 | 20% |

| ₹15,00,001 and above | 30% |

Key Changes in Deductions

- Standard Deduction: Increased for family pensioners

- Employer’s Contribution: Adjusted for NPS accounts under the new regime

- Tax Rebate: Up to ₹25,000 for taxable incomes up to ₹7 lakh

- Surcharge: No change for incomes above ₹2 crore

Old Tax Regime Overview

- Deductions: Includes Section 80C (up to ₹1.5 lakh), Section 80D (up to ₹25,000/Rs 50,000), and Section 80TTA (up to ₹10,000).

- Income Exemption Limits

- Below 60 years: ₹2.5 lakh

- 60 to 79 years: ₹3 lakh

- 80 years and above: ₹5 lakh

Conclusion

One of the best ways to enhance your financial game is by effectively using tax-saving schemes to lessen your liabilities. This will involve choosing an investment option that best fits your goals and risk appetite to accomplish tax benefits and financial growth. Whether you prefer the safety of PPF or the growth potential of ELSS, each option offers distinct advantages that apply under different conditions. Understanding these schemes empowers you to make informed decisions and ensure your investments are best optimised for tax savings and long-term returns.

Ready to save tax and grow wealth at the same time? Explore many options suitable for all types of investors on the Choice platform.

Related Blog

Many investors begin their Mutual fund journey to grow their wealth, but terms like open-end funds and closed-end funds can often be confusing. While both are regulated by SEBI, they differ in how you invest, redeem your money, and the level of flexibility they offer. Choosing the right one depends on your financial goals, investment horizon, and liquidity needs. In this article, we'll explain what an open-ended mutual fund is, what a closed-end fund is, the difference between open-ended and cl

31 July 2026

If you have ever browsed through IPO websites, you must have seen sections mentioning “Mainboard IPOs” and “SME IPOs”. They are both termed IPOs, but what is the difference between them? Understanding this difference matters, especially if you are new to investing in IPOs. In this blog, we will discuss what a Mainboard IPO and an SME IPO actually are, how they differ, the key differences in their risk characteristics and how you can apply to one through Choice. What Is a Mainboard IPO? A Mai

31 July 2026

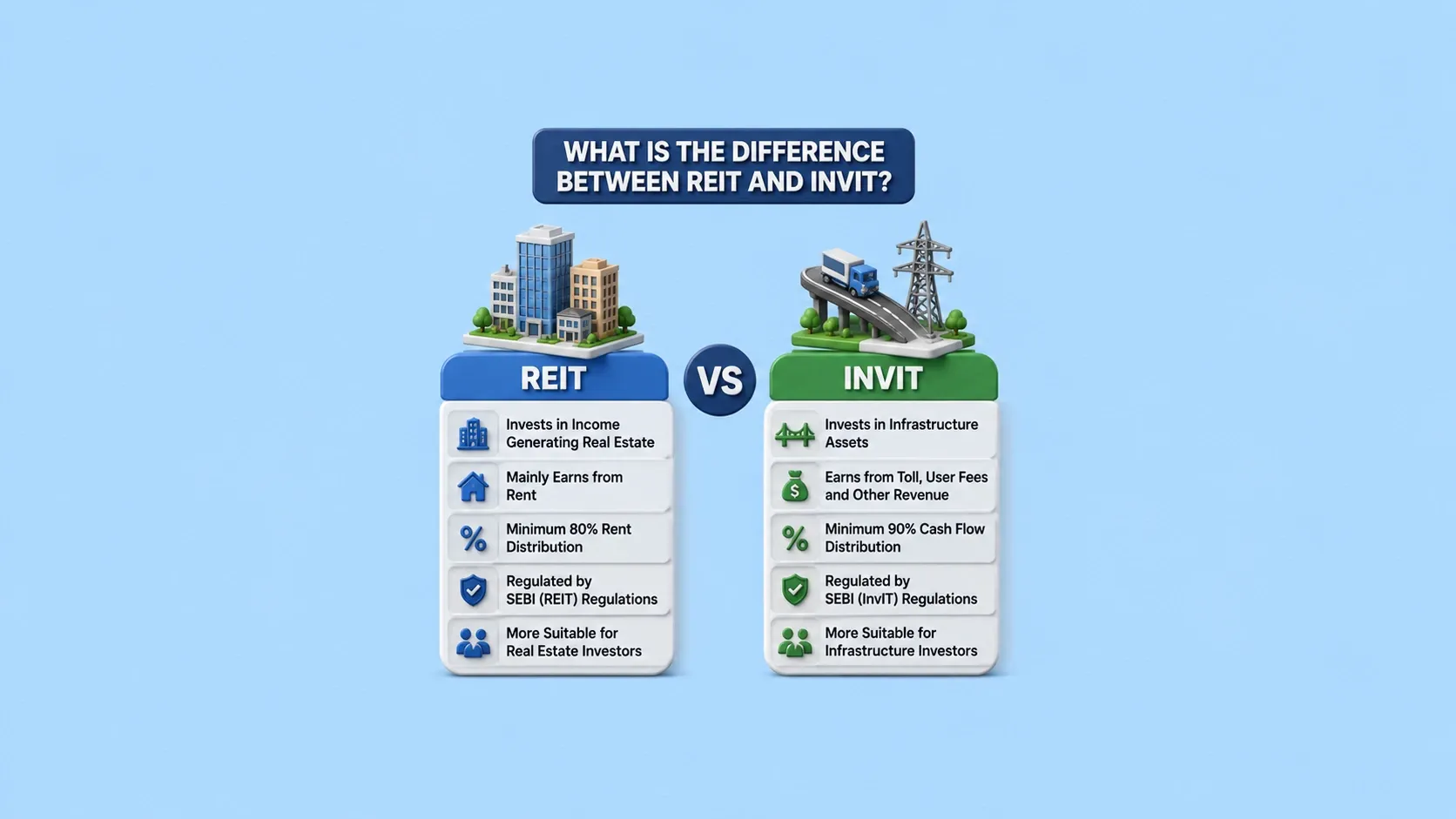

If you're looking to diversify beyond stocks, mutual funds and fixed deposits, REITs and InvITs are two investment options worth understanding. They both allow you to invest in large-scale assets such as Real Estate and infrastructure, without buying them directly. While they might have some similarity, they invest in different types of assets, carry different risk profiles and are suited for different kinds of investors. In this blog, we will learn what each instrument is, how they compare to

31 July 2026

Made for Traders.

Trusted by Investors.

Download FinX — trade confidently, invest

smarter, track everything.

Table of Contents

- Tax Saving Schemes in India: An Overview

- Top Tax Saving Schemes in India

- National Pension System (NPS)

- Tax Saving Schemes Other than 80C

- Tax Saving Investment Options for Salaried Individuals

- 100% Tax-Free Investments

- Comparison of Tax Savings Investment Options

- Latest Income Tax Slabs and Rates - FY 2025-26 | AY 2026-27

- Conclusion