When you invest in the share market or mutual funds, you receive the initial amount plus profits when you withdraw the sum if you do not incur losses. The profits accrued on this are capital gains and are subject to taxation by the Indian government.

The taxation amount depends on the nature of investments – long-term or short-term capital gain tax on shares. In most cases, investments persisting for more than 12 months fall under the umbrella of long-term holdings.

This blog will discuss how these long term holdings in the share market are taxed and the regulations that dictate the long term capital gain tax on shares in India.

What are Long Term Capital Gains in Shares?

Consider an example where you bought 10 company shares in June 2022. You can either sell this or accumulate more shares to average your holdings.

If you have maintained these shares in your portfolio for over 12 months, they are classified as long term holdings, and their profits are long-term capital gains.

But before 2018, the government levied no tax on long-term capital gains. Section 10 (38) of the Income Tax Act, 1961 granted exemption from paying taxes on long-term capital gains. So, you could sell your equity shares in the market and receive the total amount.

But with the budget for 2018, the government removed this exemption. Income from equity shares was subject to taxation, depending on the value of capital gains.

Current Taxation Rules for Long Term Capital Gains On Shares

Budget 2018 introduced Section 112A in the Income Tax Act of 1961, implementing a uniform taxation module on equities, mutual funds related to equities and business trust funds.

It was decided that the tax on long term capital gain on shares was to be capped at 10%, along with the cess. But the tax was only applicable on gains made above INR 1,00,000. So, if your income or profits from shares is less than INR 1,00,000 per annum, you are not liable for tax cuts.

Exemptions

Even with the taxation on long term capital gains, there are several cases where you can be exempt or pay a reduced fee. Some of the exemptions, as defined under Section 54F, are provided below:

- If you are between 60 to 80 years of age, the limit of capital gains without incurring taxes is INR 3,00,000 per annum.

- Suppose the capital gains from shares are reinvested into a residential property. But if you sell the residential property within three years of purchase, the tax exemption will no longer be applicable.

In these cases, you are not liable to pay any taxes on your gains. But the value of reinvestment also decides your tax liabilities. Here are two cases to better illustrate it:

- If you reinvest the entire capital gains amount, the tax will be exempt completely

- If you only decide to reinvest a part of your gains, the exemption will be calculated per a standard formula.

Exemption = (Capital gains acquired x price of the new house)/ Net consideration value

The Addition of Grandfathering

Immediately after the Budget 2018 declared a long-term capital gain tax on shares in India, the grandfather rule was invoked.

The roots of grandfathering paint it as a concept where the old rules apply in some instances while the new regulations are applied to future cases.

Essentially, it meant that profits for taxation would only be considered after 1st February 2018. So, all the gains made from shares before 31st January 2018 were safe from tax. It emerged as a reliable method to benefit taxpayers in the old regime and protect their income.

How to Calculate the Long Term Capital Gain Tax On Shares

Before you calculate the capital gain tax accrued from your shares, it is necessary to define some values:

- The total value of the sale (A)

- Cost of acquisition or the initial amount paid for the shares (B)

- Long-term capital gains (A – B)

- Time of holding (more than one year for long-term gains)

- Fixed tax rate of 10%

So, the total tax liability can be calculated by ascertaining the 10% of long-term capital gains. For example, if the capital gains accrued are INR 1,50,000, the total tax liability is INR 15,000.

Final Thoughts

With the rise in the popularity of the stock market, capital gains from shares have added a boost to the economy.

In most cases, it is easy to calculate the amount owed by multiplying the capital gain amount by 10%. However, you can also apply for exceptions by reinvesting in a residential property for three years or more.

But with the grandfather rule in place, you will not incur taxes on any profits gained before 31st January 2018. So, keep that in mind while filing your taxes and enjoy minimum tax cuts on your gains!

FAQ

What is the formula for calculating long term capital gain tax on shares?

The first step is to define the total amount gained after selling the shares (A) and the initial investment (B). Subtracting A and B will give you the capital gain accrued. If this figure is higher than INR 1,00,000, then your tax liability will be 10% of the total profits.

What is a long-term capital gain exemption on shares?

You can get exemptions in one of two cases.

- If you are between 60 to 80 years of age and have capital gains below INR 3,00,000 per year

- The amount reinvested into a residential property

How much tax do I pay on long term capital gain 112A?

According to 112A, you have to pay a tax of 10% if the long-term capital gains exceed the amount of INR 1,00,000 in a fiscal year.

Related Blog

Many investors begin their Mutual fund journey to grow their wealth, but terms like open-end funds and closed-end funds can often be confusing. While both are regulated by SEBI, they differ in how you invest, redeem your money, and the level of flexibility they offer. Choosing the right one depends on your financial goals, investment horizon, and liquidity needs. In this article, we'll explain what an open-ended mutual fund is, what a closed-end fund is, the difference between open-ended and cl

31 July 2026

If you have ever browsed through IPO websites, you must have seen sections mentioning “Mainboard IPOs” and “SME IPOs”. They are both termed IPOs, but what is the difference between them? Understanding this difference matters, especially if you are new to investing in IPOs. In this blog, we will discuss what a Mainboard IPO and an SME IPO actually are, how they differ, the key differences in their risk characteristics and how you can apply to one through Choice. What Is a Mainboard IPO? A Mai

31 July 2026

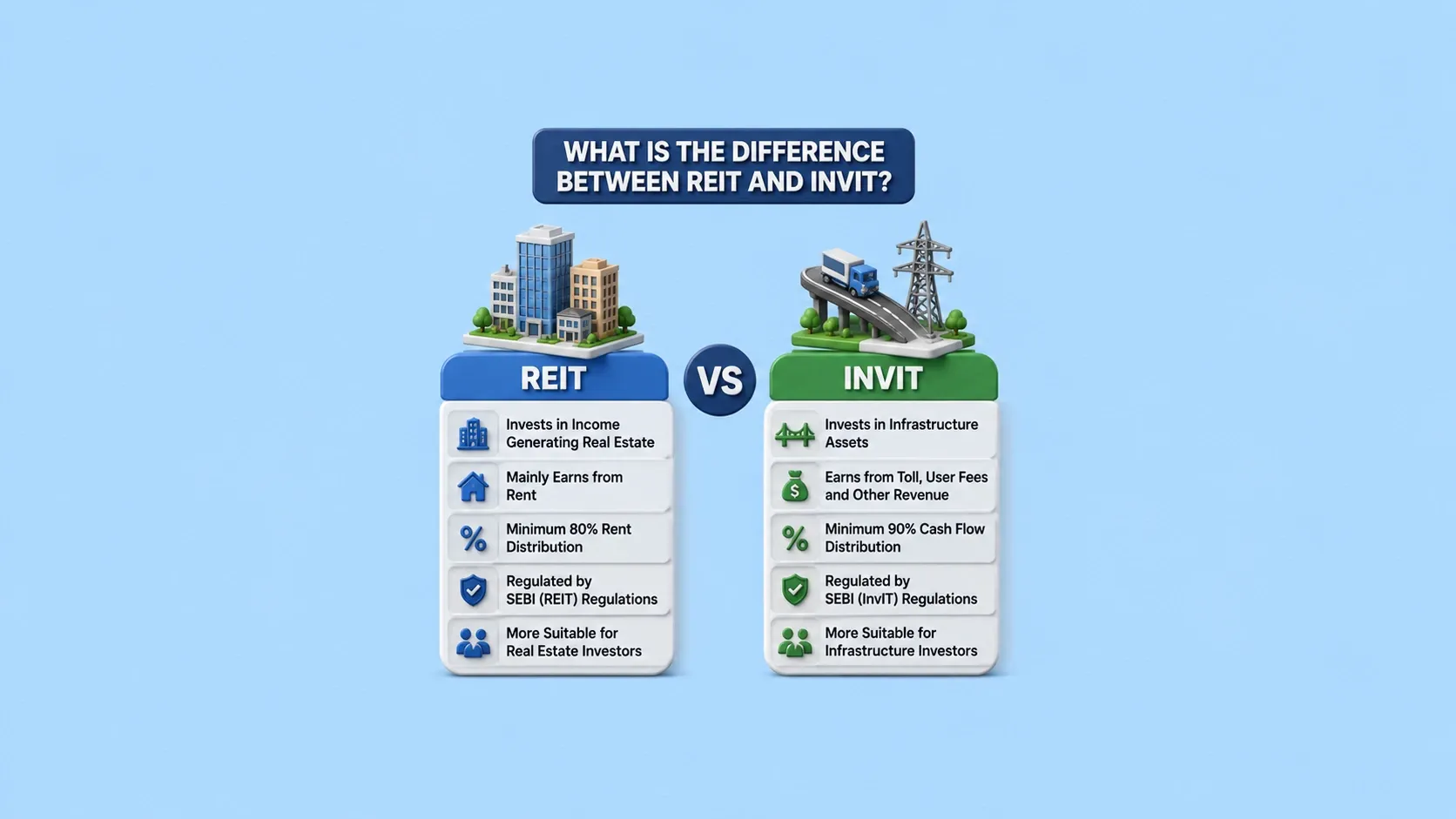

If you're looking to diversify beyond stocks, mutual funds and fixed deposits, REITs and InvITs are two investment options worth understanding. They both allow you to invest in large-scale assets such as Real Estate and infrastructure, without buying them directly. While they might have some similarity, they invest in different types of assets, carry different risk profiles and are suited for different kinds of investors. In this blog, we will learn what each instrument is, how they compare to

31 July 2026

Made for Traders.

Trusted by Investors.

Download FinX — trade confidently, invest

smarter, track everything.