India’s defence sector has emerged as one of the most dynamic and strategically vital industries in the country, driven by a confluence of geopolitical realities, policy reforms, and economic imperatives. With the government’s unwavering focus on self-reliance through initiatives like Atmanirbhar Bharat and record-breaking defence budgets, this sector presents a compelling investment thesis. For retail and institutional investors alike, defence-sector mutual funds offer a pathway to participate in this growth story while navigating its inherent risks. This analysis explores the structural drivers of India’s defence industry, evaluates the performance and composition of leading mutual funds in this space, and contextualises recent geopolitical developments that underscore the sector’s long-term relevance.

India’s Defence Sector: A Macroeconomic Pillar of Growth

Policy-Led Transformation

India’s defence sector has undergone a paradigm shift since 2014, transitioning from import dependency to strategic autonomy. The government allocated ₹6.81 lakh crore (USD 78.3 billion) to defence in the 2025–26 budget, a 9.5% year-on-year increase and the highest-ever capital outlay. This surge is underpinned by the Atmanirbhar Bharat initiative, which reserves 75% of procurement budgets for domestic manufacturers. As a result, indigenous defence production skyrocketed to ₹1.27 lakh crore in FY 2023–24, marking a 174% increase since 2014–15. Concurrently, defence exports surged from ₹686 crore (USD 81 million) in 2013–14 to USD 2.51 billion in 2023–24, with a target of USD 5.95 billion by 2029.

Infrastructure and Industrial Base

Two dedicated Defence Industrial Corridors in Uttar Pradesh and Tamil Nadu now anchor an ecosystem of over 350 major manufacturers and 10,000+ MSMES. Public sector giants like Hindustan Aeronautics Limited (HAL) and Bharat Electronics Limited (BEL) dominate this landscape, but private players such as Tata Advanced Systems and Larsen & Toubro are gaining prominence through joint ventures and technology transfers. The sector’s modernisation drive includes a USD 130 billion procurement plan over the next 5–7 years, focusing on fighter jets, naval vessels, missiles, and AI-driven systems.

Geopolitical Catalysts and Recent Developments

Rising Regional Tensions

The Pahalgam terror attack (April 2025) and India’s retaliatory Operation Sindoor (May 2025) have intensified focus on military readiness. The latter involved precision strikes on 11 Pakistani airbases and nine terror camps using Rafale jets armed with SCALP missiles, underscoring India’s evolving combat capabilities. Such incidents validate the government’s push for indigenisation, as reliance on foreign suppliers during crises risks operational vulnerabilities.

Global Arms Race Dynamics

Global defence spending reached USD 2.2 trillion in 2024, driven by the Russia-Ukraine war, U.S.-China tech rivalry, and instability in the Indo-Pacific. India, straddling contested borders with China and Pakistan, is leveraging this environment to position itself as a “net security provider” in the Indian Ocean Region (IOR). The recent commissioning of the indigenously built INS Vikrant aircraft carrier and Project 75 submarines exemplifies this ambition.

Defence Mutual Funds: Vehicles for Strategic Exposure

Fund Landscape and Performance

As of May 2025, four primary mutual funds dominate the defence thematic space:

| Fund | AUM (₹ Cr) | Expense Ratio | 1-Year Return* |

|---|---|---|---|

| HDFC Defence Fund (Direct-Growth) | ₹5,487 Cr | 1.80% | 20.15% |

| Motilal Oswal Nifty Defence Index Fund | ₹2,875 Cr | 1.08% | 24.13% (6 months) |

| Aditya Birla SL Nifty Defence Fund | ₹461 Cr | 1.06% | 23.54% (6 months) |

*Data as of May 2025

HDFC Defence Fund, the largest active fund, has delivered 49% annualised returns since its 2023 inception, outperforming the Nifty 50’s 8–10% in the same period. Its portfolio leans heavily on HAL (19.79%), BEL (18.53%), and Solar Industries (16.01%). Passive funds like Motilal Oswal’s Nifty Defence Index Fund replicate the Nifty India Defence Index, which surged 20–30% in early 2025 amid border tensions and budget announcements

Portfolio Composition and Trends

Defence funds typically invest across three verticals:

- Aerospace: HAL, BEL, and Tata Advanced Systems (drone tech).

- Shipbuilding: Mazagon Dock, Cochin Shipyard, Garden Reach Shipbuilders.

- Ordnance and Tech: Bharat Dynamics (missiles), Astra Microwave (radars), Paras Defence (satellite tech).

Notably, 75% of the Nifty Defence Index is concentrated in large caps, mitigating mid-cap volatility. The sector’s valuation premium-P/E ratios of 35–40 versus Nifty 50’s 22-reflects growth expectations but warrants caution during market corrections.

Risks and Strategic Considerations

Sector-Specific Challenges

- Policy Dependency: Defence budgets and procurement cycles are subject to political priorities. Delays in projects like the ₹62,700 crore LCH Prachand helicopter order could impact revenue visibility.

- Export Risks: While India aims to export USD 5.95 billion by 2029, geopolitical alliances and competition from established players like Israel and South Korea pose hurdles.

- Valuation Volatility: The Nifty Defence Index’s 12-month beta of 1.3 indicates higher volatility than broader markets.

Investor Guidance

- Horizon: A minimum 5–7-year holding period is advised to ride out cyclicality.

- Allocation: Limit exposure to 5–10% of equity portfolios, using SIPs to average entry costs.

- Monitoring: Track defence budget announcements, export orders, and geopolitical developments.

Conclusion: Aligning Capital with National Priority

India’s defence sector stands at an inflexion point, buoyed by unprecedented government support, technological advancements, and a precarious global order. For investors, thematic mutual funds offer a structured avenue to capitalise on this momentum. While the HDFC Defence Fund’s active management has delivered stellar returns, passive index funds provide low-cost diversification. However, the sector’s inherent risks-policy shifts, execution delays, and valuation froth demand disciplined investing.

Recent events like Operation Sindoor underscore the non-negotiable imperative of military modernisation, ensuring sustained demand for domestic defence products. As India transitions from the world’s largest arms importer to a burgeoning exporter, its defence equities could mirror the growth trajectories of South Korea’s Hanwha or Israel’s Elbit Systems. For those with risk appetite and patience, defence mutual funds are not merely financial instruments but stakes in India’s strategic future.

“In a world where security is the new currency, investing in defence is investing in sovereignty”

Related Blog

Many investors begin their Mutual fund journey to grow their wealth, but terms like open-end funds and closed-end funds can often be confusing. While both are regulated by SEBI, they differ in how you invest, redeem your money, and the level of flexibility they offer. Choosing the right one depends on your financial goals, investment horizon, and liquidity needs. In this article, we'll explain what an open-ended mutual fund is, what a closed-end fund is, the difference between open-ended and cl

31 July 2026

If you have ever browsed through IPO websites, you must have seen sections mentioning “Mainboard IPOs” and “SME IPOs”. They are both termed IPOs, but what is the difference between them? Understanding this difference matters, especially if you are new to investing in IPOs. In this blog, we will discuss what a Mainboard IPO and an SME IPO actually are, how they differ, the key differences in their risk characteristics and how you can apply to one through Choice. What Is a Mainboard IPO? A Mai

31 July 2026

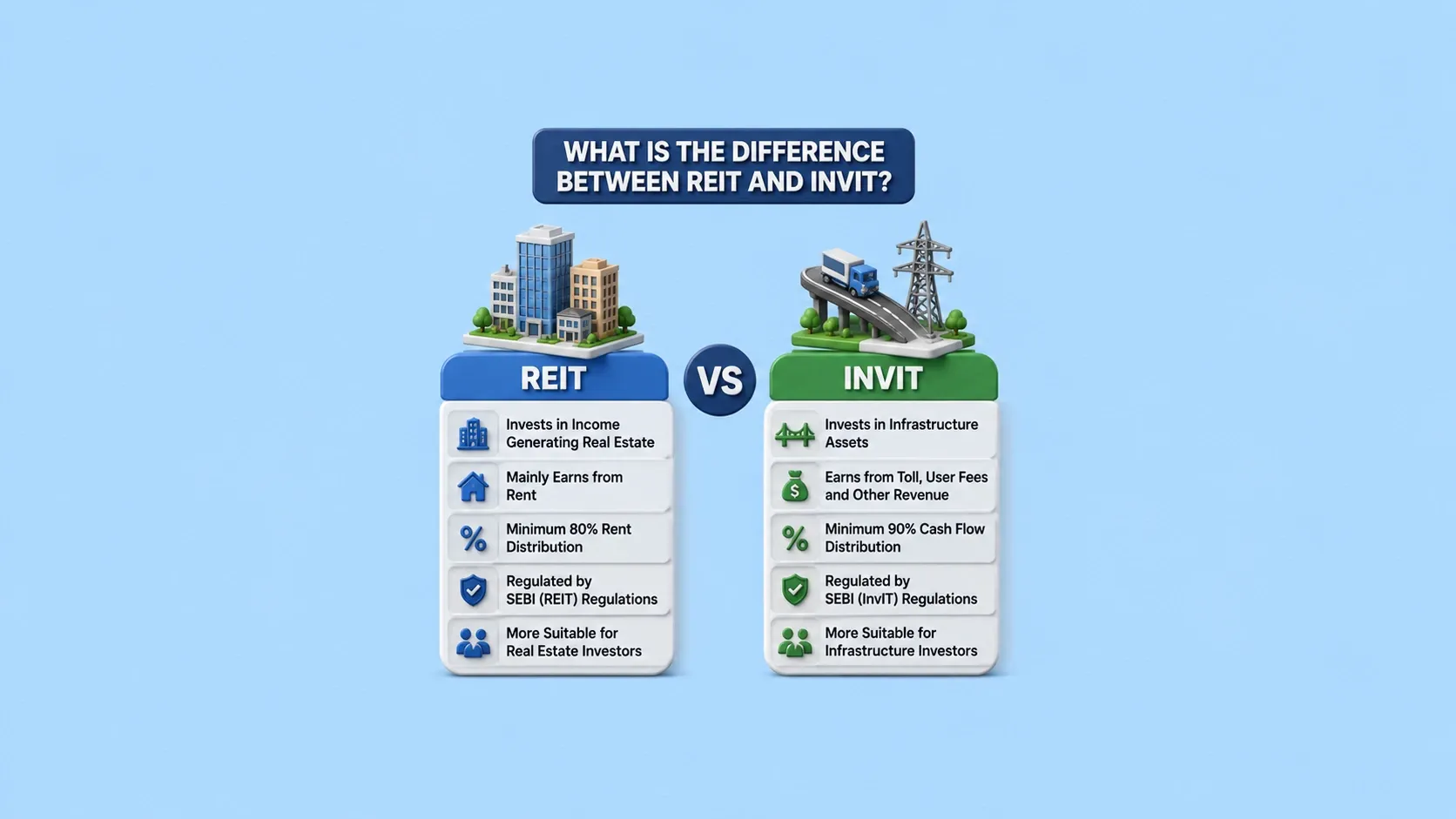

If you're looking to diversify beyond stocks, mutual funds and fixed deposits, REITs and InvITs are two investment options worth understanding. They both allow you to invest in large-scale assets such as Real Estate and infrastructure, without buying them directly. While they might have some similarity, they invest in different types of assets, carry different risk profiles and are suited for different kinds of investors. In this blog, we will learn what each instrument is, how they compare to

31 July 2026

Made for Traders.

Trusted by Investors.

Download FinX — trade confidently, invest

smarter, track everything.