Investors always seek ways to lessen tax burdens and further increase wealth. There are investment options with tax benefits that also have the potential to yield long-term returns.

The two most well-known investment options that can help someone achieve these goals in India are the Equity Linked Savings Schemes and Systematic Investment Plans. While both ELSS and SIPs have their advantages, you must understand their main differences to make the right choice.

This article discusses the differences between ELSS and SIP in terms of their features, benefits, and shortcomings.

What is ELSS?

The Equity-Linked Savings Scheme is basically a mutual fund with the primary investment in equities. ELSS is one of the well-known tax-saving investment options with a lock-in period of just 3 years, the shortest among tax-saving options.

ELSS is unique because of its tax efficiency. ELSS provides provisions to claim deductions up to Rs. 1,50,000 under Sec 80C per financial year (for the old tax regime). ELSS holds greater potential to yield higher returns than other avenues to invest in for saving on your taxes, such as the Public Provident Fund, National Savings Certificate, and tax-saving fixed deposits.

The ELSS scheme is handy for long-term financial planning and often yields returns superior to the inflation rate. Yet, you should not forget that there is a market risk in ELSS funds, too, and the value of such funds fluctuates with the equity market's performance.

| Pros | Cons |

|---|---|

| Tax deductions up to Rs. 1,50,000 under Section 80C. | Investment value fluctuates with market performance. |

| Only a 3-year lock-in period, the shortest among tax-saving options. | Higher risk compared to debt-based instruments. |

| Possibility of higher returns compared to traditional tax-saving investments. | Returns can be unpredictable due to market fluctuations. |

| Can provide growth that outpaces inflation. | May have higher management fees compared to other tax-saving investments. |

ELSS scheme has been historically proven to be a wealth creator if you stay invested in the scheme long after the lock-in period:

Here is how ELSS compares to other interest-saving schemes:

What is SIP?

You can invest in mutual funds either as a lump sum or on a recurring basis. A Systematic Investment Plan (SIP) refers to a method whereby you regularly invest a fixed sum of money in mutual funds. This will allow you to accumulate wealth over time without stressing about market timing or making one significant investment.

SIP works on the power of compounding: a small, regular investment grows with interest and returns over time. You can invest every week, month, quarter, or even twice a year. The time-frequency is solely your decision. You are also free to choose how much to invest each time, more than the minimum set by the fund house. SIP could be an ideal choice if you are a new investor or looking for a disciplined savings mode.

| Pros | Cons |

|---|---|

| Encourages regular, consistent investments. | Investments are subject to market fluctuations. |

| Regular investments grow over time through compounding. | Returns are not guaranteed and can fluctuate. |

| You can adjust the investment amount as per your financial situation. | May incur management fees and other charges. |

| Allows you to invest small amounts periodically instead of a large lump sum. | Some funds have a minimum lock-in period, which might affect liquidity. |

Comparison of ELSS Vs SIP

ELSS is a type of mutual fund scheme you can invest in while investing in SIP is a way to invest in any mutual fund scheme (including ELSS) that lets you benefit from rupee cost averaging. A comparison between the two is given below so that you can understand the differences between ELSS and SIP:

| Aspect | ELSS | SIP |

|---|---|---|

| Investment Type | Mutual fund with a focus on equities. | Investment method for mutual funds. |

| Tax Benefits | Tax deductions up to Rs. 1,50,000 under Section 80C. | No direct tax benefits, depending on the fund's nature. |

| Lock-in Period | 3 years, the shortest among tax-saving options. | No lock-in period for SIPs; depends on the mutual fund. |

| Investment Frequency | Lump sum investment or through SIP. | Regular investments (weekly, monthly, quarterly, or semi-annually). |

| Investment Amount | Can be a lump sum or regular SIP investments. | Flexible; you choose the amount to invest regularly. |

| Return Potential | Higher potential returns due to equity exposure. | Returns depend on the mutual fund's performance and market conditions. |

| Compounding Benefits | Benefits from the power of compounding over the lock-in period. | Compounding benefits through regular investments over time. |

| Market Risk | High; subject to equity market fluctuations. | High; subject to the mutual fund's underlying assets. |

| Management Fees | Usually moderate; depends on the fund. | Typically lower compared to lump sum investments. |

| Liquidity | Limited liquidity due to a 3-year lock-in. | Generally more liquid; depends on the mutual fund's terms. |

| Flexibility | Limited flexibility; locked-in for 3 years. | Highly flexible; adjust or stop investments as needed. |

| Suitability | Ideal for tax-saving and long-term growth. | Suitable for disciplined saving and regular investments. |

ELSS or SIP – Which is Better?

ELSS schemes provide investors with regular tax-saving opportunities and save them from the last-minute rush of tax planning. SIPs in ELSS would inculcate a disciplined saving habit with the benefit of rupee cost averaging, thereby maximising returns.

ELSS and SIP are two different concepts under mutual funds, and it may not be appropriate to compare these as it is akin to comparing apples and oranges. The best thing is to combine the merits of both.

The chart below shows how ELSS final corpus differs based on whether you invested in lumpsum or through SIP:

Though SIPs offer more flexibility, ELSS is considered better because of its tax benefit. Savvy investors often use SIP to invest in ELSS funds to gain maximum advantage.

Also Read: Difference Between ULPS and ELSS

Taxation for ELSS

ELSS is a widely preferred mutual fund option mainly for its tax benefits despite the three-year lock-in period:

Tax Benefits During Investment

Under Section 80C, the deduction for investment made in ELSS is allowed up to ₹1.5 lakh in the financial year when the investment was started.

Also Read: Top 3 tax saving Mutual funds

Taxation on Redemption

As mentioned earlier, ELSS has a compulsory lock-in period of three years, after which all the gains are categorised as Long-Term Capital Gains (LTCG).

- Tax-Free Upto ₹1 Lakh: LTCG made from ELSS up to ₹1 lakh in a single financial year is exempted from income tax.

- LTCG over Rs.1 lakh: LTCG earned over Rs.1 lakh shall be taxed at 10%.

Example: If you invest ₹1 lakh in an ELSS fund in any financial year, you are allowed to claim exemption from paying income tax on ₹1 lakh. After three years, say if the growth in your investment has crossed ₹1.5 lakh, you will pay a 10% tax on the ₹50,000 profit.

Remember, the ELSS funds primarily invest in equity stocks. Thus, this category is fairly susceptible to market volatility.

Also Read: Are Elss Taxable After 3 Years

Conclusion

ELSS and SIP both have their merits in the eyes of investors regarding tax-saving and investment growth prospects. Whereas ELSS will extend the benefit of tax deduction and give higher returns, SIPs are a disciplined mode of investment, which can help multiply your money over time. Which will be the best for you? That depends on your financial goal, time horizon, and risk tolerance. Yields from ELSS and SIP plans vary, reflecting market performance.

Begin your investment journey today to secure your financial future. Explore Choice to find ELSS schemes with exciting returns and tax savings. You can invest in these schemes through a lumpsum investment or SIPs.

Related Blog

Many investors begin their Mutual fund journey to grow their wealth, but terms like open-end funds and closed-end funds can often be confusing. While both are regulated by SEBI, they differ in how you invest, redeem your money, and the level of flexibility they offer. Choosing the right one depends on your financial goals, investment horizon, and liquidity needs. In this article, we'll explain what an open-ended mutual fund is, what a closed-end fund is, the difference between open-ended and cl

31 July 2026

If you have ever browsed through IPO websites, you must have seen sections mentioning “Mainboard IPOs” and “SME IPOs”. They are both termed IPOs, but what is the difference between them? Understanding this difference matters, especially if you are new to investing in IPOs. In this blog, we will discuss what a Mainboard IPO and an SME IPO actually are, how they differ, the key differences in their risk characteristics and how you can apply to one through Choice. What Is a Mainboard IPO? A Mai

31 July 2026

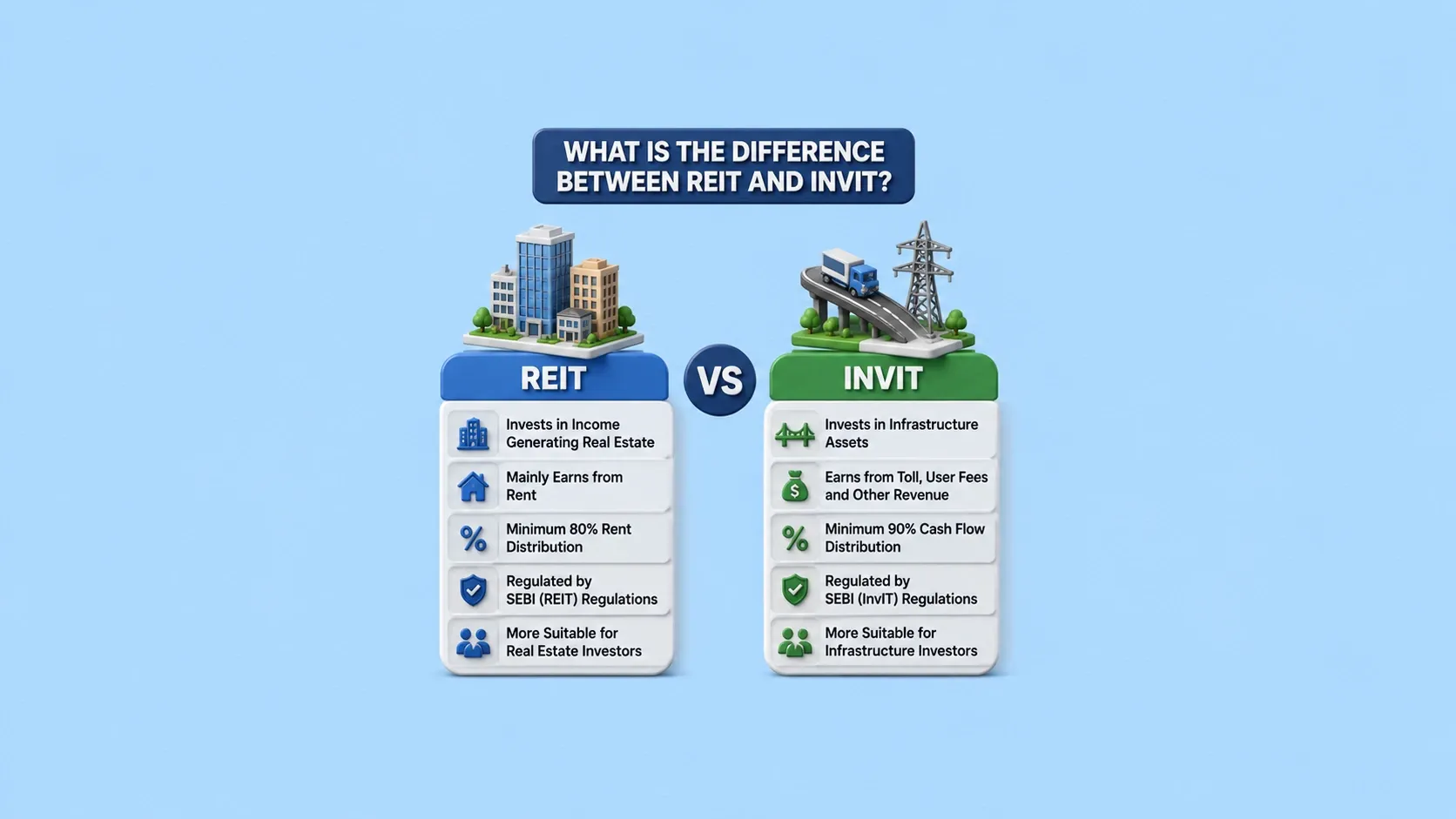

If you're looking to diversify beyond stocks, mutual funds and fixed deposits, REITs and InvITs are two investment options worth understanding. They both allow you to invest in large-scale assets such as Real Estate and infrastructure, without buying them directly. While they might have some similarity, they invest in different types of assets, carry different risk profiles and are suited for different kinds of investors. In this blog, we will learn what each instrument is, how they compare to

31 July 2026

Made for Traders.

Trusted by Investors.

Download FinX — trade confidently, invest

smarter, track everything.